.jpg)

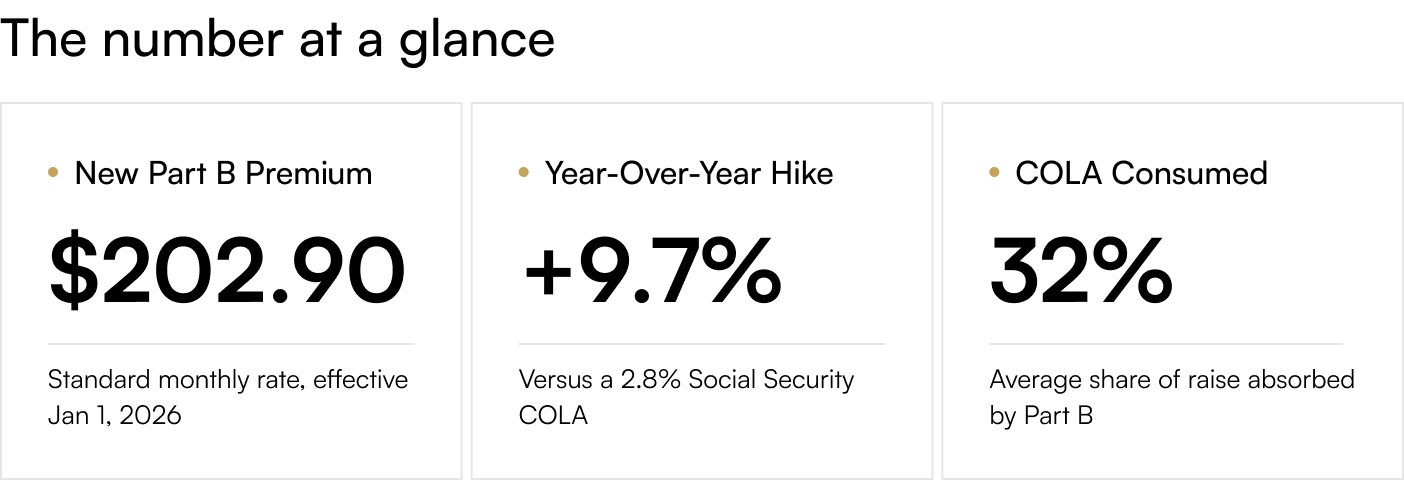

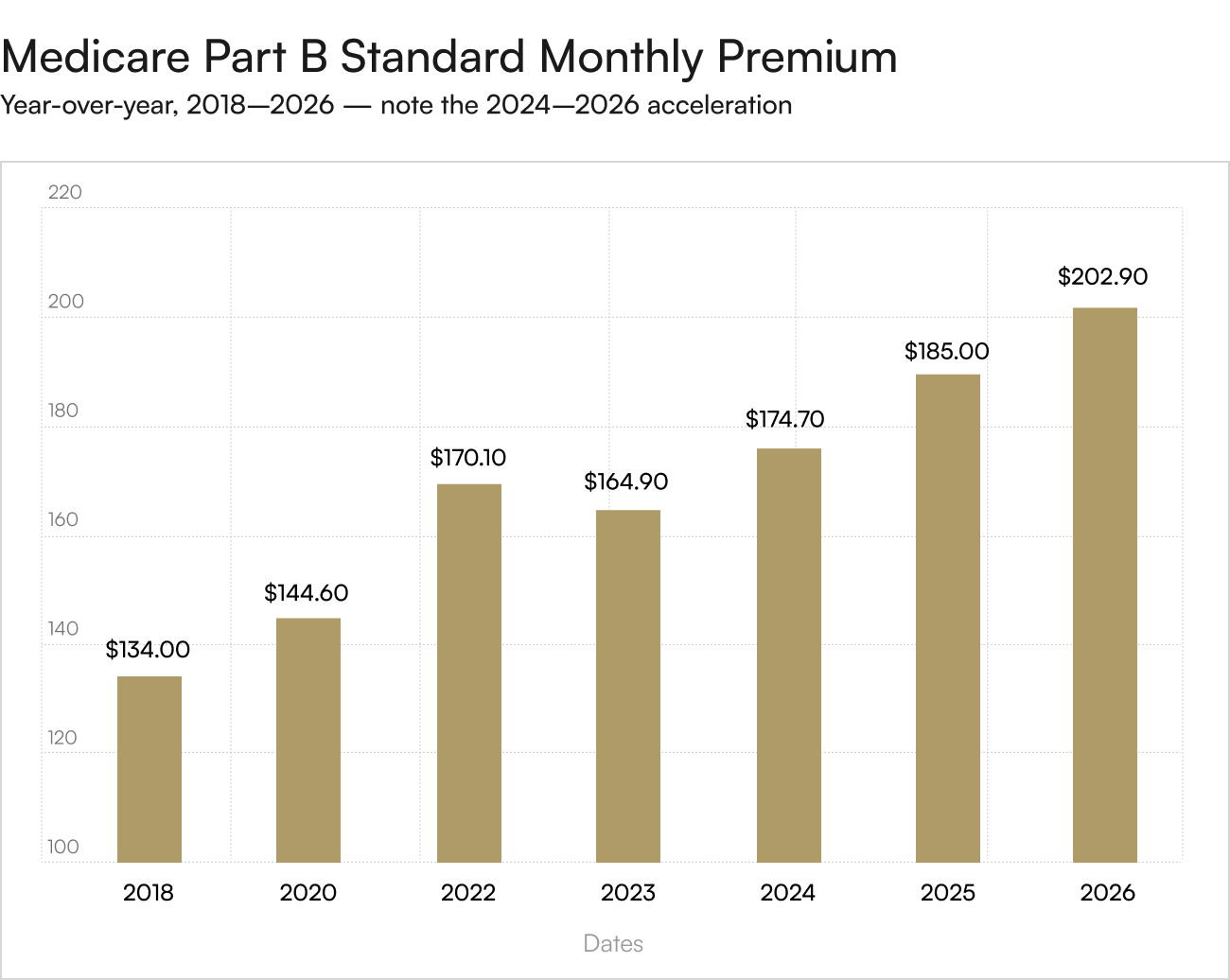

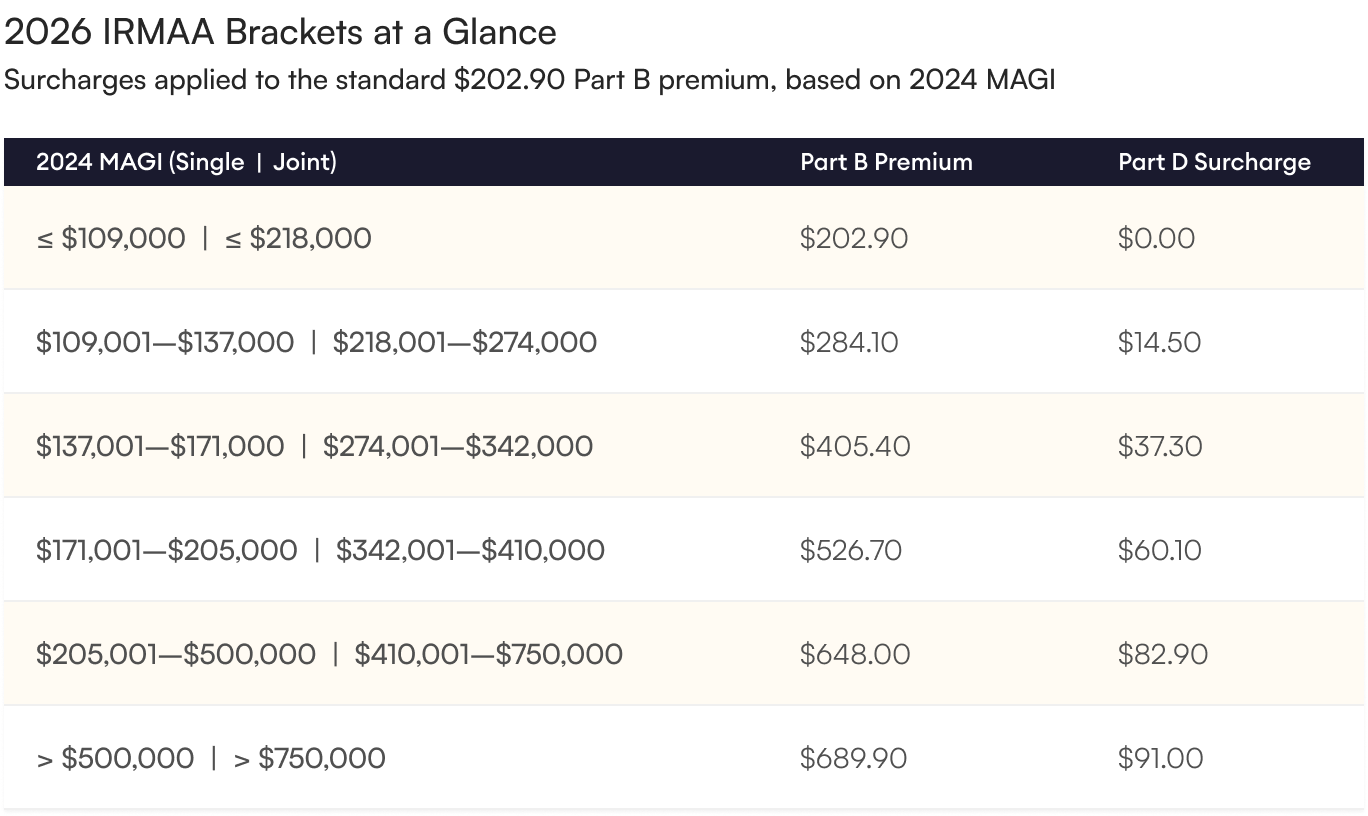

On November 14, 2025, the Centers for Medicare & Medicaid Services confirmed the 2026 Medicare premium schedule, and the numbers tell a story that every Social Security recipient should understand. The standard monthly Part B premium rises from $185.00 to $202.90 — a $17.90 monthly jump, or 9.7% year-over-year. The annual Part B deductible climbs to $283 from $257, and the inpatient Part A deductible moves to $1,736. For higher-income retirees, the income-related monthly adjustment amount (IRMAA) pushes the effective Part B premium to anywhere from $284.10 to $689.90 per month, depending on bracket.

In the same announcement window, the Social Security Administration confirmed the 2026 cost-of-living adjustment at 2.8%, raising the average retired-worker check by approximately $56 per month. The arithmetic is unforgiving: a $56 raise minus a $17.90 Part B increase leaves the typical retiree with roughly $38 of new monthly income. Roughly 32% of the COLA is consumed before it reaches the bank account — and that figure does not yet include Medicare Part D inflation, Medigap premium increases, or the higher cost-sharing baked into Original Medicare's revised deductible structure.

The 2026 increase marks the third consecutive year that Part B has outpaced the COLA in raw dollar terms — a structural pattern, not an anomaly.

Why This Is Structurally Bad for Retirees

Healthcare is not a one-time expense. It compounds. The Center for Retirement Research at Boston College projects that the Part B premium as a share of the average Social Security benefit will reach 9.4% in 2026 — an all-time high — up from 8.3% in 2018 and roughly 6.0% at the turn of the century. Medicare trustees further project Part B premium growth averaging 6.4% annually from 2027 through 2031, comfortably above projected COLAs and headline inflation. This is what economists describe as stealth income erosion: nominal benefits rise, but real spending power shrinks because mandatory deductions grow faster than the increases that ostensibly compensate for inflation.

IRMAA: The Tax You Did Not Know You Owed

For higher-income retirees, the standard Part B premium is just the floor. The income-related monthly adjustment amount layers on additional charges that can more than triple the monthly cost. Critically, IRMAA is calculated using a two-year look-back: 2026 surcharges are based on the modified adjusted gross income reported on a retiree's 2024 federal tax return. That means a one-time event in 2024 — a Roth conversion, the sale of a long-held property, a large traditional-IRA withdrawal, an inherited-IRA distribution — can quietly inflate a 2026 Medicare bill by thousands of dollars, often as a complete surprise.

The two-year look-back creates an underappreciated planning problem. A retiree who executes a five-figure Roth conversion in 2024 to manage long-term tax exposure may receive a Medicare bill in early 2026 that adds more than $5,800 to the household's healthcare costs for that year alone. This is precisely the dynamic that argues for keeping a portion of wealth in assets that do not generate annual taxable income. Physical gold held in a self-directed IRA generates no taxable distributions until the account holder elects to take one. Physical gold held in a taxable brokerage or storage account produces no dividends or interest that flow onto the Form 1040 and lift the AGI.

The Compounding Hidden Cost

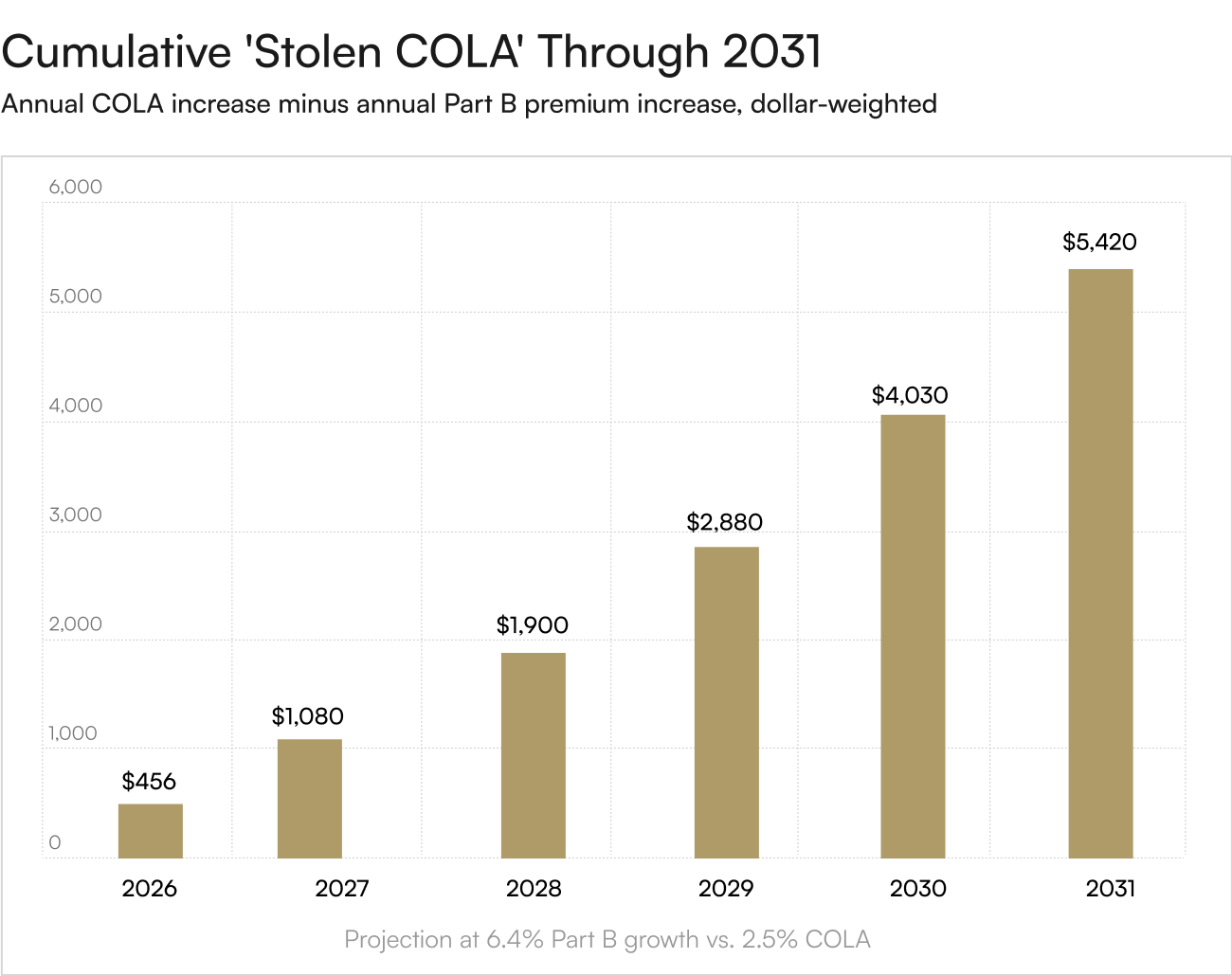

Consider a 67-year-old retiree whose Social Security check rises $56 in 2026 and whose Part B premium rises $17.90. He keeps roughly $38 per month, or $456 over the year. If Part B continues to grow at the trustees' projected 6.4% annual rate and COLAs run at the long-run 2.5% average, the cumulative 'stolen COLA' by 2031 will exceed $5,400. Over a 20-year retirement, the figure compounds into a five-figure transfer from the retiree's general budget to the federal healthcare program — money that the COLA was nominally designed to protect.

Gold as the Asset That Is Not Indexed to a Bureaucracy

Between May 2025 and May 2026, gold's price moved from approximately $3,335 to $4,732 per troy ounce — a 41% year-over-year advance. Gold does not have a CMS rule-making cycle. It does not have IRMAA. It does not have a hold-harmless clause that depends on whether a particular retiree's Social Security check is large enough. For retirees concerned about their COLA being steadily reabsorbed by federal healthcare inflation, an allocation to physical precious metals functions as an external hedge — one not subject to the pricing decisions of any single federal agency or congressional committee.

The structural argument is not that gold replaces Medicare; nothing replaces Medicare. The argument is that the same household that is forced to absorb hidden 9.7% Medicare premium increases should also hold a non-correlated reserve asset capable of growing well above the CMS inflation curve. Over the trailing 12 months, gold has done exactly that, and the long-run institutional forecasts from Goldman Sachs, JPMorgan, and UBS — all converging in the $5,400–$6,000 range — suggest the trend has further to run.

Medicare premiums will continue climbing faster than Social Security COLAs through at least 2031 — that pattern is now baked into the trustees' own projections. The household that absorbs this transfer year after year without offsetting it elsewhere is losing real purchasing power on a schedule. To explore how a precious-metals allocation can sit outside the IRMAA system and protect the real value of your retirement income, the advisers at Merchant Gold Group can structure a Precious Metals IRA strategy calibrated to your specific tax and benefit situation, with no obligation and no pressure.