.jpg)

The largest intergenerational wealth transfer in American history is now underway. Cerulli Associates' most recent estimate, released in early 2026, projects that approximately $84 trillion will pass from the Baby Boomer generation to their heirs and to charitable beneficiaries between now and 2045. A substantial share of that wealth — likely more than $12 trillion — sits in traditional individual retirement accounts. The rules for inheriting those accounts changed dramatically with the SECURE Act of 2019, and after a four-year transition period in which the IRS waived its own enforcement mechanisms, those rules began being enforced in 2025. Many of the heirs now squarely in the new regime do not yet realize the position they are in.

From Stretch IRA to Compressed Drawdown

Before 2020, a non-spouse beneficiary who inherited a traditional IRA could 'stretch' distributions over their own life expectancy. That structure produced two important results. First, it allowed the inherited balance to compound tax-deferred for decades, often spanning a beneficiary's full career. Second, it spread the tax bill across many years, frequently keeping the heir in a lower marginal bracket than they would otherwise occupy. The stretch IRA was, in practical terms, one of the most powerful estate-planning vehicles available to American families.

The SECURE Act eliminated the stretch for most non-spouse beneficiaries inheriting on or after January 1, 2020. Under the new rule, those beneficiaries must fully empty the inherited account within ten years of the original owner's death. Then, in July 2024, the IRS finalized regulations resolving years of confusion about whether annual required minimum distributions are mandated during the ten-year window. The answer, in most cases, is yes: if the original owner had already begun their own lifetime RMDs before death, the heir must take annual RMDs in years 1 through 9 and fully deplete the account by the end of year 10.

The IRS waived enforcement of the annual-RMD requirement from 2021 through 2024 to give beneficiaries time to adjust. The grace period ended in 2025. The clock is now running for real.

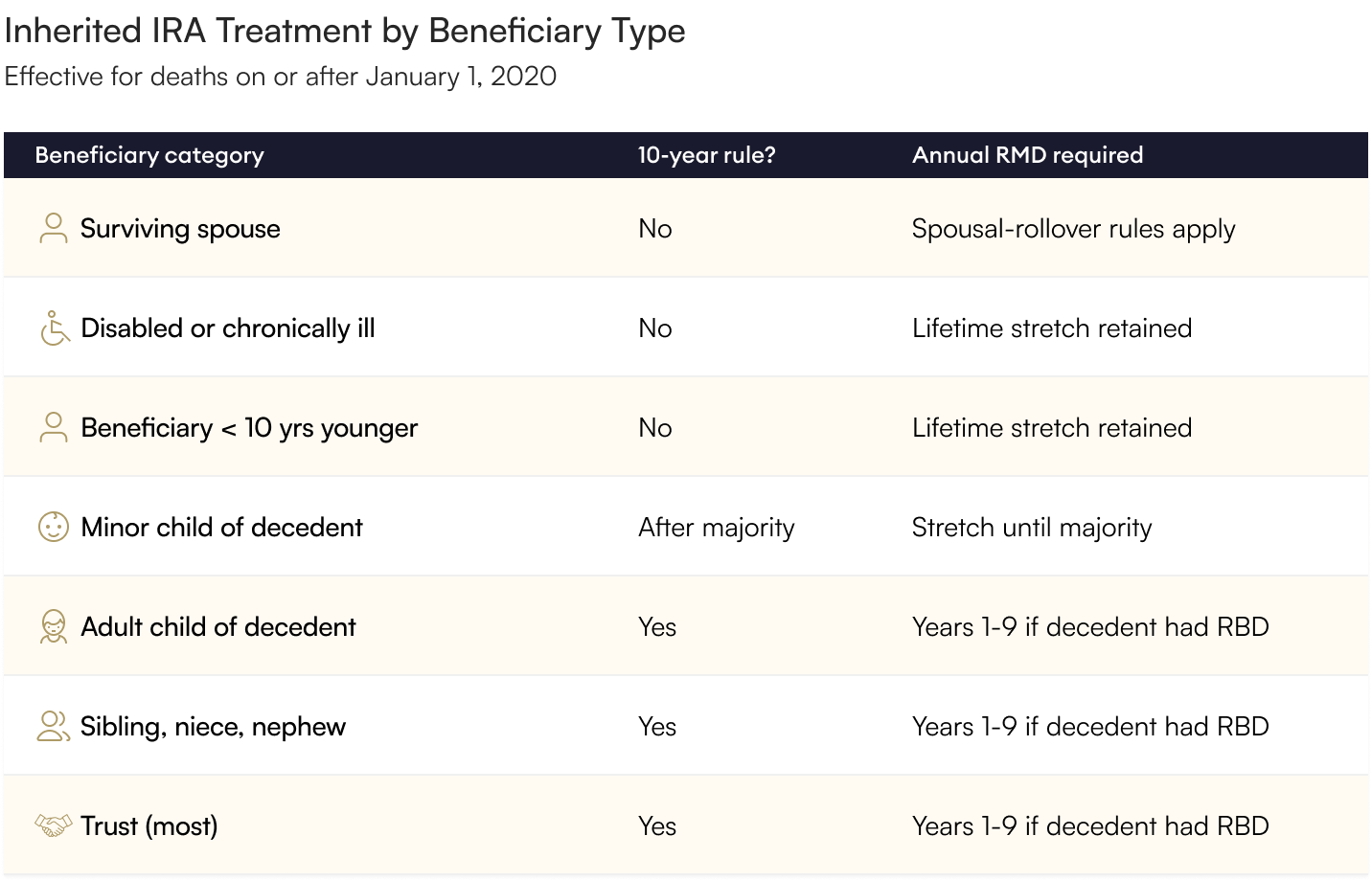

Who Escapes — and Who Is Caught

Five categories of beneficiary remain exempt from the new ten-year regime and can continue stretching distributions over their lifetimes: surviving spouses, beneficiaries who are disabled, beneficiaries who are chronically ill, beneficiaries not more than ten years younger than the decedent, and minor children of the decedent (though the minor's stretch ends at the age of majority, at which point the ten-year clock begins). Everyone else — adult children, siblings, nieces, nephews, partners not legally married, and most non-qualifying trusts — falls squarely into the ten-year rule.

The Tax-Stacking Problem

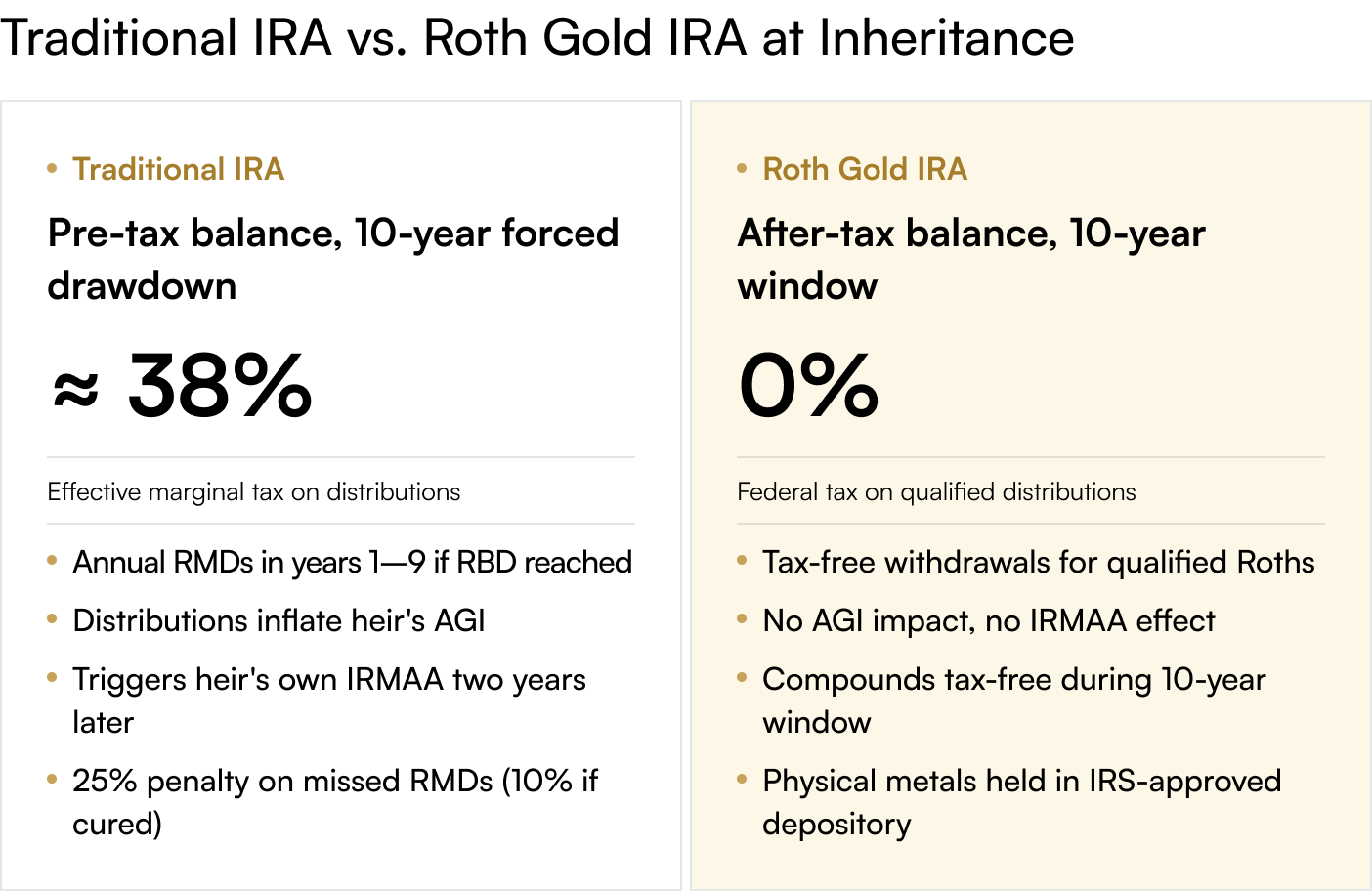

The deeper problem with the new regime is not the ten-year window itself; it is the way the compressed distribution schedule interacts with the heir's existing income. Traditional inherited IRA distributions are fully ordinary income. Consider a 53-year-old physician inheriting a $1.2 million traditional IRA from a parent who passes away in 2026. Spread evenly across ten years, the inherited balance generates roughly $120,000 of additional taxable income annually — typically arriving at the peak of the heir's earning life. That additional income frequently pushes the heir into the 32% or 35% federal bracket, increases her own IRMAA exposure two years later, restricts certain itemized deductions, and may eliminate eligibility for Roth contributions she had otherwise been making.

In practice, the math gets worse than the headline rate suggests. A 32% federal bracket combined with a 6% state bracket, layered with FICA-equivalent surcharges and lost deduction phase-outs, produces an effective marginal cost on inherited-IRA distributions that frequently exceeds 40%. On a $1.2 million traditional IRA, that translates into nearly $500,000 of cumulative taxes over the ten-year drawdown — a transfer the original account owner almost certainly did not intend at the scale that now applies.

Why Gold Reshapes the Inheritance Math

The combination of the SECURE Act's compressed timeline and the IRS's 2025 enforcement posture has materially changed the relative attractiveness of different asset locations for legacy planning. Physical gold held in a Roth IRA that has met the five-year and age-59½ requirements before the original owner's death passes to non-spouse heirs subject to the ten-year rule — but the distributions are generally tax-free rather than ordinary income. That single difference can preserve hundreds of thousands of dollars on a high-six- or seven-figure inheritance.

Physical gold held in a regular taxable account passes with a step-up in basis at death under current law, potentially eliminating decades of unrealized capital gains. A parent who purchased gold at $1,800 per ounce in 2020 and dies in 2030 with gold at, say, $7,500 per ounce, would have a $5,700 per-ounce unrealized gain wiped clean. The heir inherits at the date-of-death valuation. If they sell shortly thereafter, the taxable gain is minimal or zero. This is the single largest tax-efficient mechanism still available to high-net-worth families under current law.

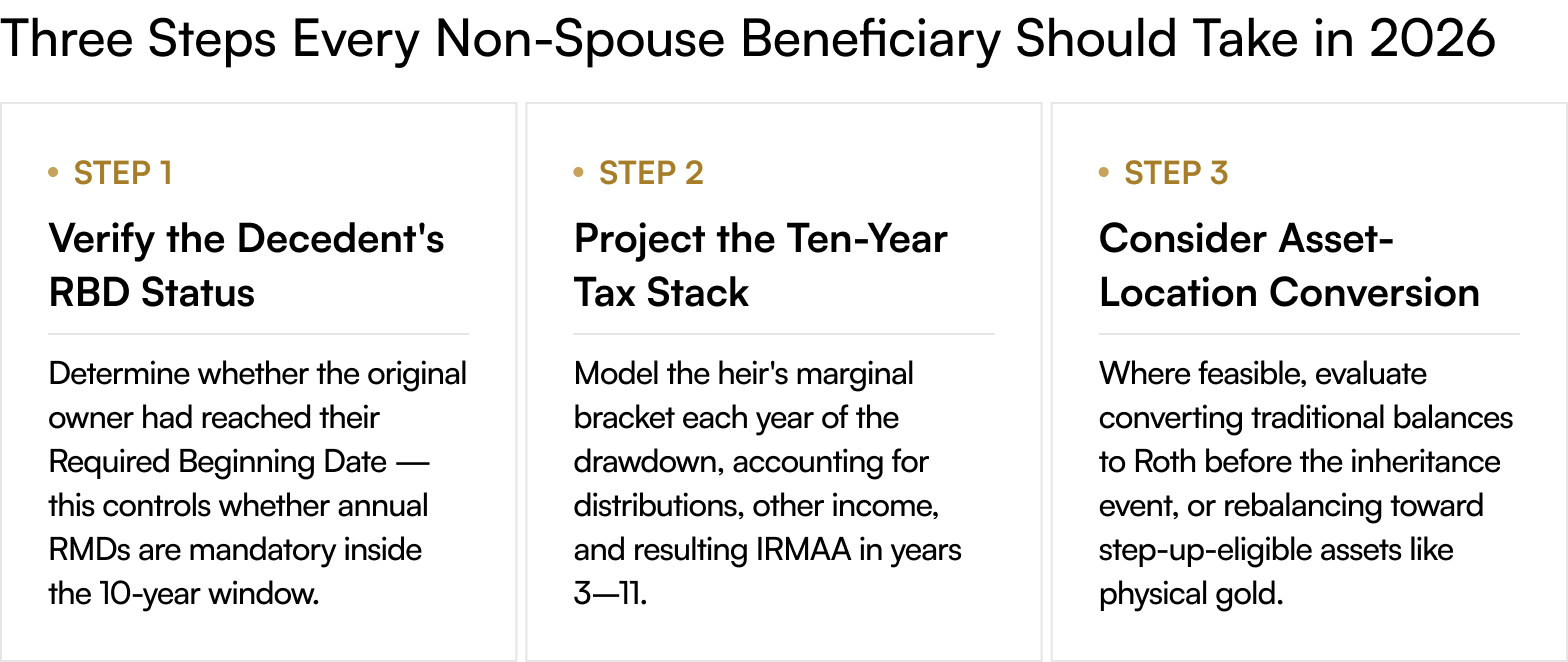

A Practical Heir's Checklist

The ten-year clock is already ticking for millions of American heirs, and the IRS is no longer issuing waivers. The window to reshape an estate plan for the new rules is finite, but it is still open for households where the original account owner is alive and able to act. To understand how a Roth precious-metals IRA or step-up-eligible taxable gold holding could meaningfully reduce the tax friction your heirs will face under the SECURE Act regime, the legacy-planning team at Merchant Gold Group can perform a confidential review of your current beneficiary structure and walk you through the specific mechanics that apply to your situation. The consultation is complimentary and there is no obligation.