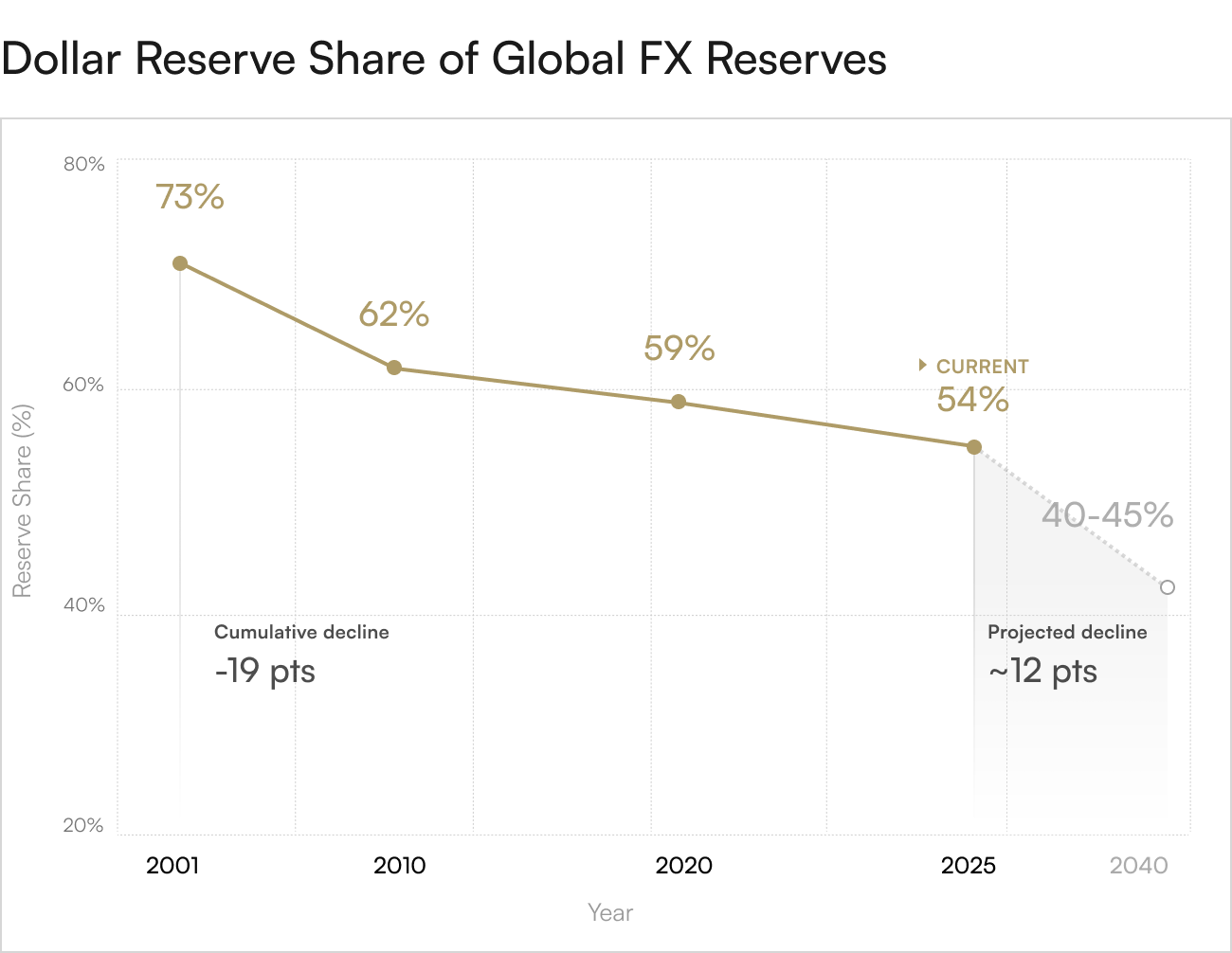

In 2001, the U.S. dollar represented 73% of global foreign exchange reserves, a position of unrivaled monetary dominance. As of 2025, that share has collapsed to approximately 54%, according to IMF COFER data. This 19 percentage point decline represents the most significant erosion of reserve currency status since the fall of the British pound in the mid 20th century. The proximate cause is clear: the United States has weaponized the dollar and the SWIFT international payment system to impose financial sanctions on adversaries, freezing hundreds of billions in sovereign assets and cutting nations off from the global financial infrastructure. The unintended consequence has been a mass exodus from dollar reserves toward gold, the only asset immune to confiscation, sanctions, or geopolitical coercion.

The Sanctions Era

Geopolitical tensions, particularly the Russia Ukraine war and other conflicts, led to the deployment of financial sanctions on an unprecedented scale. Russia had approximately $300 billion in foreign exchange reserves frozen by Western governments. Russian banks were ejected from SWIFT, the messaging system that underpins cross border payments. Iranian oil revenues were blocked. Venezuelan state assets were seized. While these measures were intended to coerce adversaries and protect American interests, they often failed to achieve their policy goals and instead demonstrated to every non aligned nation that holding dollar reserves creates existential vulnerability. If the United States can freeze your central bank's assets overnight for geopolitical reasons, those reserves are not truly yours.

Gold Fills the Void

Central banks have responded to dollar weaponization by accumulating gold at the fastest pace since the end of the Bretton Woods system. Gold's share of global central bank reserves is now at its highest level since 1991, approximately 30%, while the dollar's share is at its lowest since 1994. In 2025, central banks purchased 863 tonnes of gold, and projections for 2026 indicate purchases of 755 tonnes. A World Gold Council survey found that 95% of central banks expect to increase their gold reserves in 2026. This is not a coincidence. Gold cannot be frozen. Gold cannot be sanctioned. Gold cannot be weaponized against its holder. Gold is the ultimate sovereign reserve asset in a multipolar world where trust in the hegemon has collapsed.

The Emerging Reserve Mix

As the dollar's reserve share declines, other assets are gaining ground. The euro holds approximately 20% of reserves, but the eurozone's own structural issues limit its appeal. The Chinese yuan has grown to roughly 2.5% to 3% of reserves, but capital controls and lack of deep bond markets constrain broader adoption. The real winner is gold, which offers liquidity, universal acceptance, and zero political risk. Analysts project that in a gradual de-dollarization scenario, the dollar's reserve share could fall to 40% to 45% by 2040, with the difference reallocated primarily to gold and a basket of alternative currencies.

What This Means for the United States

Reserve currency status confers enormous economic privileges. The United States can borrow at lower rates because global demand for Treasuries is structurally embedded in the reserve system. The U.S. can run persistent trade deficits because other nations need to accumulate dollars. The U.S. can export inflation by printing dollars that are absorbed into foreign central bank reserves. As reserve status erodes, all of these advantages diminish. Borrowing costs rise. Trade deficits become less sustainable. Inflation becomes harder to export and easier to import. Retired General Mark Milley, former Chairman of the Joint Chiefs of Staff, acknowledged in 2023 that the dollar's dominance may indeed be threatened. Western policy circles have been reluctant to accept this reality, but the evidence mounts daily.

The Dollar Decline Is Your Portfolio's Problem

American retirement investors often assume that because they live in the United States and spend dollars, currency risk does not apply to them. This is a dangerous misconception. As the dollar loses reserve status, its purchasing power declines. Imported goods become more expensive. Inflation becomes more persistent. Treasury yields rise to compensate foreign buyers for currency risk, increasing government borrowing costs and reducing fiscal space. The very stability that made dollar assets attractive erodes. Gold, by contrast, is not a currency issued by any government. It is a stateless, apolitical asset whose value does not depend on any nation's fiscal discipline or geopolitical goodwill. As central banks dump dollars for gold, retirement investors would be wise to follow their lead.

Diversify Out of Dollar Dependence

The decline in the dollar's reserve share from 73% to 54% is not a blip; it is a structural trend that will define the next two decades of global finance. Central banks understand this, which is why they are accumulating gold at record levels. Retirement portfolios overweight in dollar denominated stocks, bonds, and cash are making an unhedged bet that the dollar will reverse this decline and reclaim its dominance. That bet grows riskier every day. Physical gold and silver held in a self directed Precious Metals IRA offer a way to diversify out of exclusive dollar dependence and into an asset that benefits from the very trend that threatens fiat currencies. Contact Merchant Gold Group today to learn how to position your retirement savings for a world where the dollar is no longer the unquestioned king of global finance and gold reclaims its throne as the ultimate store of sovereign wealth.