For decades, the 60/40 portfolio — sixty percent stocks, forty percent bonds — was the default retirement model for U.S. households. The logic was elegant: equities provided long-term growth, while bonds delivered steady income and acted as a shock absorber when stocks fell. From the early 1980s through the late 2010s, the model worked roughly as advertised.

Then 2022 happened. Both stocks and bonds fell at the same time, and the 60/40 portfolio recorded one of its worst calendar years on record. The years since have offered some recovery, but the underlying problem the 2022 drawdown revealed has not been resolved: when inflation rises and rates rise with it, stocks and bonds can lose value together. The bonds, in other words, stop being a hedge.

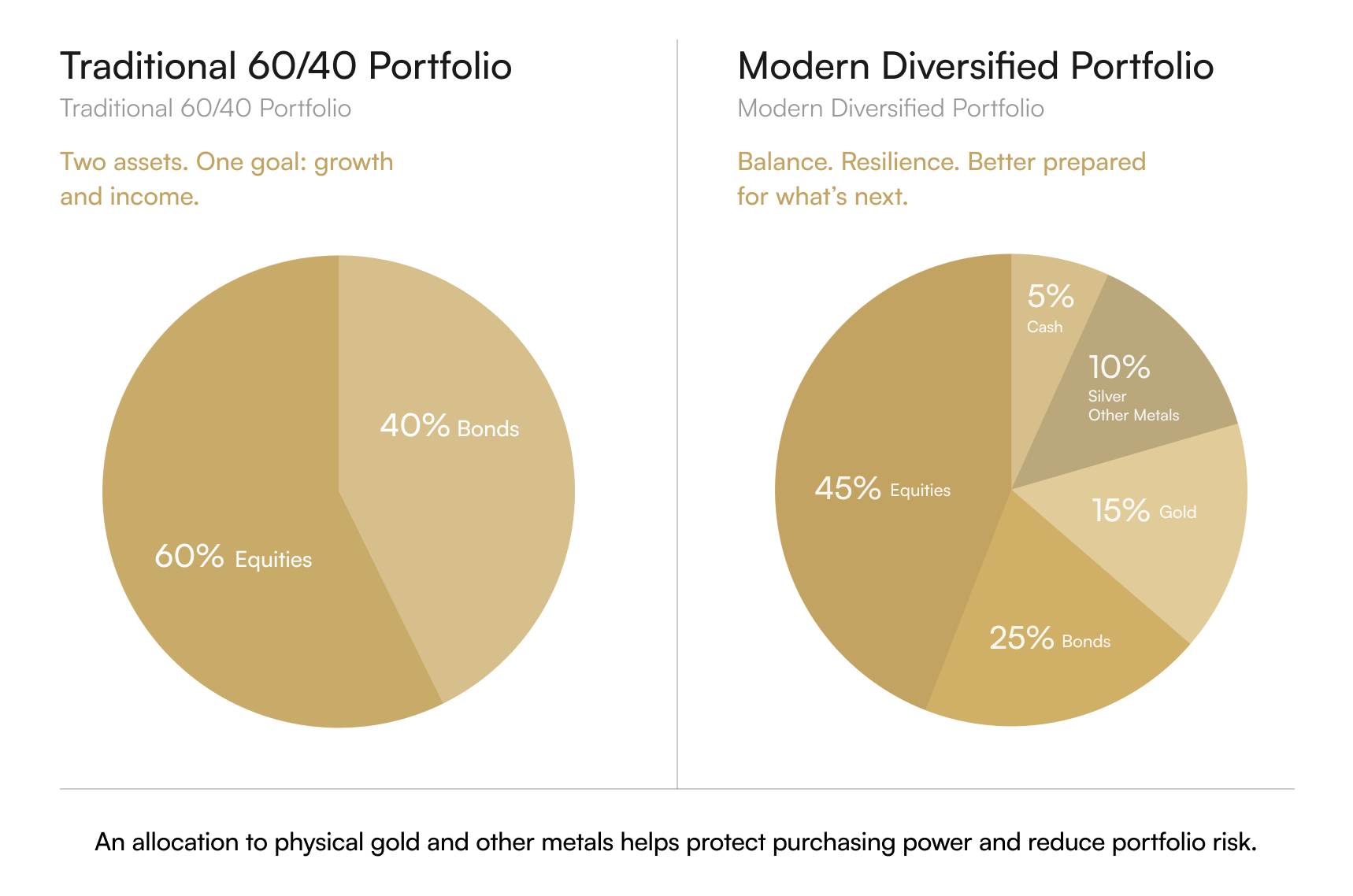

What Actually Broke

The 60/40 model relied on a structural negative correlation between equities and high-quality fixed income — when stocks fell, bonds typically rose, smoothing the overall portfolio path. That correlation held for most of a forty-year period during which inflation was generally falling and policy rates were trending lower.

The current environment is different. U.S. national debt has crossed thirty-seven trillion dollars, fiscal deficits run at six to seven percent of GDP, and the Federal Reserve has been forced into an awkward dance between fighting inflation and avoiding a recession. In that backdrop, bonds are exposed to two simultaneous risks: the price risk from rising yields, and the purchasing-power risk from sticky inflation. Neither risk is hedged by holding more bonds.

Why Gold Behaves Differently

Physical gold has no counterparty, no coupon, and no underlying business operations. That makes it an unappealing comparison to a stock or a bond on most metrics — but those same characteristics are what make it useful in a retirement portfolio.

Gold has historically performed during the precise scenarios that damage diversified financial portfolios: persistent inflation, currency debasement, sovereign credit stress, and geopolitical fragmentation. It is uncorrelated, on a long enough timeframe, to both stocks and bonds. And because it is a tangible asset held outside the banking system, it provides a layer of resilience that paper assets — including gold ETFs and mining stocks — cannot.

“Gold's job in a retirement portfolio is not to make you rich. Its job is to make sure you survive the years that try to make you poor.”

What a Modern Allocation Looks Like

Most institutional and family-office models that have updated their thinking since 2022 carry between five and fifteen percent in precious metals, with the largest share in gold. A representative modern allocation for a near-retiree might look like forty-five percent global equities, twenty-five percent shorter-duration bonds and inflation-linked instruments, fifteen percent physical gold, ten percent silver and other metals, and five percent cash. The exact numbers vary with risk tolerance, but the structural change is consistent: bonds give up some share, and physical metals take a permanent seat at the table.

Crucially, the metals portion is best held physically rather than through paper proxies. Gold ETFs offer convenience and tradability, but they reintroduce the counterparty exposure and financial-system dependency that gold was added to solve. Bullion held by a credible custodian, or coins held personally, accomplish the original purpose more directly.

How Retirement Accounts Can Hold Physical Metals

This is the part most savers do not realize is available to them. The IRS permits self-directed IRAs to hold physical gold, silver, platinum, and palladium, provided the products meet specific fineness standards and are held by an approved depository. Existing 401(k) and traditional IRA balances can be rolled over into a precious-metals IRA without triggering a taxable event. The tax treatment of the underlying account — traditional or Roth — is preserved through the rollover.

That structure allows a retiree to hold real, physical bullion inside a tax-advantaged retirement wrapper. It is one of the most powerful tools available for the kind of portfolio repair the post-2022 environment demands, and it remains underused largely because most savers were never told it existed.

What does it mean for you? The 60/40 model served a generation, but the conditions it was built for no longer hold. If you are evaluating how a measured precious-metals position could rebalance your IRA, 401(k), or after-tax retirement savings, request a no-cost consultation with Merchant Gold Group to review the rollover process, IRS-approved products, and storage options that fit your timeline.