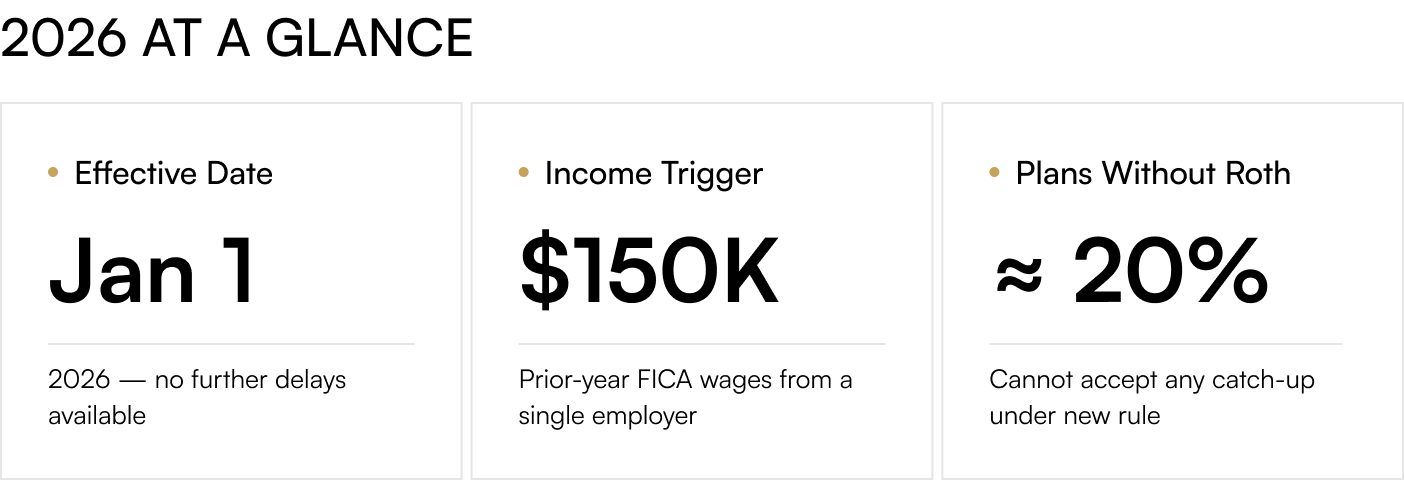

For three consecutive years, the retirement-plan industry lobbied the Treasury for delays. The lobbying is over. Effective January 1, 2026, under SECURE 2.0 Section 603 and the final regulations the Internal Revenue Service issued on September 16, 2025, employees aged 50 or older whose prior-year FICA wages from a single employer exceeded $150,000 must make any 401(k), 403(b), or governmental 457(b) catch-up contributions on a Roth (after-tax) basis. Pre-tax catch-up contributions are no longer an option for this group. The mandate represents one of the largest practical changes to American retirement-plan mechanics in a generation, and many participants and even some plan sponsors are not yet fully prepared.

The 2026 Contribution Architecture

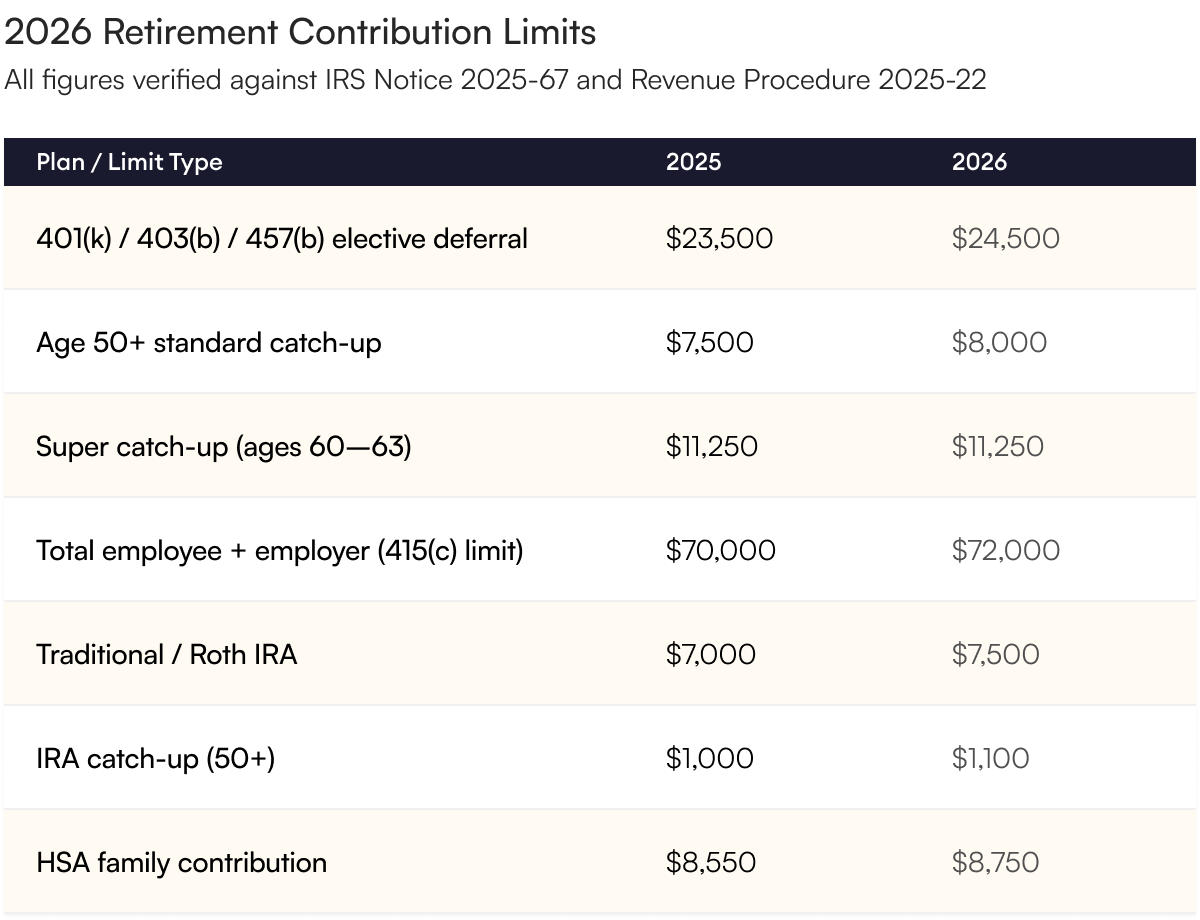

Before turning to who is affected and what it costs, the new contribution limits themselves should be in the foreground of every household plan. The IRS confirmed inflation-adjusted figures for 2026 in November 2025; they are the operating numbers any 50-plus saver must work from this year.

Who Is Captured by the Rule — and Who Is Not

The new rule is narrower than headline coverage often suggests. A saver who earned $150,001 in FICA wages from a single employer in 2025 is captured. A saver who earned $149,999 is not, and can continue making pre-tax catch-up contributions. Several quirks deserve explicit attention because they create either legitimate planning opportunities or unintended exclusions:

- The threshold uses FICA wages — Social Security wages reported on the W-2 — not adjusted gross income, not total compensation. Bonus deferrals, certain pretax benefits, and partnership distributions can leave a high earner technically below the threshold.

- The threshold applies per employer. A saver who exceeded $150,000 across two jobs is not automatically captured at either; the rule must trip at a single employer.

- A worker who started a new job on January 1, 2026 is exempt for 2026 even if they earned $1,000,000 at their prior employer in 2025 — because the prior-year wages came from a different employer.

- If a 401(k) plan does not offer a Roth feature, captured high earners are prohibited from making catch-up contributions at all. Industry surveys put the share of plans without a Roth feature at roughly 20%, meaning many high earners will simply lose access to catch-ups in 2026.

The Real Tax Cost of the Mandate

Pre-tax catch-up contributions historically delivered an immediate tax deduction at peak earning-years marginal rates — frequently 32% or 35% federal, plus state. Forcing those dollars Roth means the saver pays tax on the contribution today at those high rates in exchange for tax-free growth and tax-free withdrawals later. That trade is mathematically sensible only if the saver expects higher tax rates in retirement than they pay today. Given the $37 trillion federal debt load, the 2032 OASI exhaustion timeline, and the demographic curve discussed in Article 1, that bet is increasingly common — but it is a bet, not a certainty.

For a 55-year-old in the 35% bracket maximizing the catch-up every year through age 64, the forced Roth treatment represents roughly $25,000 of foregone current-year deductions over the decade. Whether that cost is recovered through future tax-free withdrawals depends on three variables outside the saver's control: federal tax rates in 20 years, state tax rates in 20 years, and the saver's own marginal bracket in retirement. Two of those three variables are trending in directions that favor the Roth — and that is the rational case for the mandate, even if the immediate cost feels punitive.

Why a Self-Directed Roth Precious-Metals IRA Now Makes More Sense

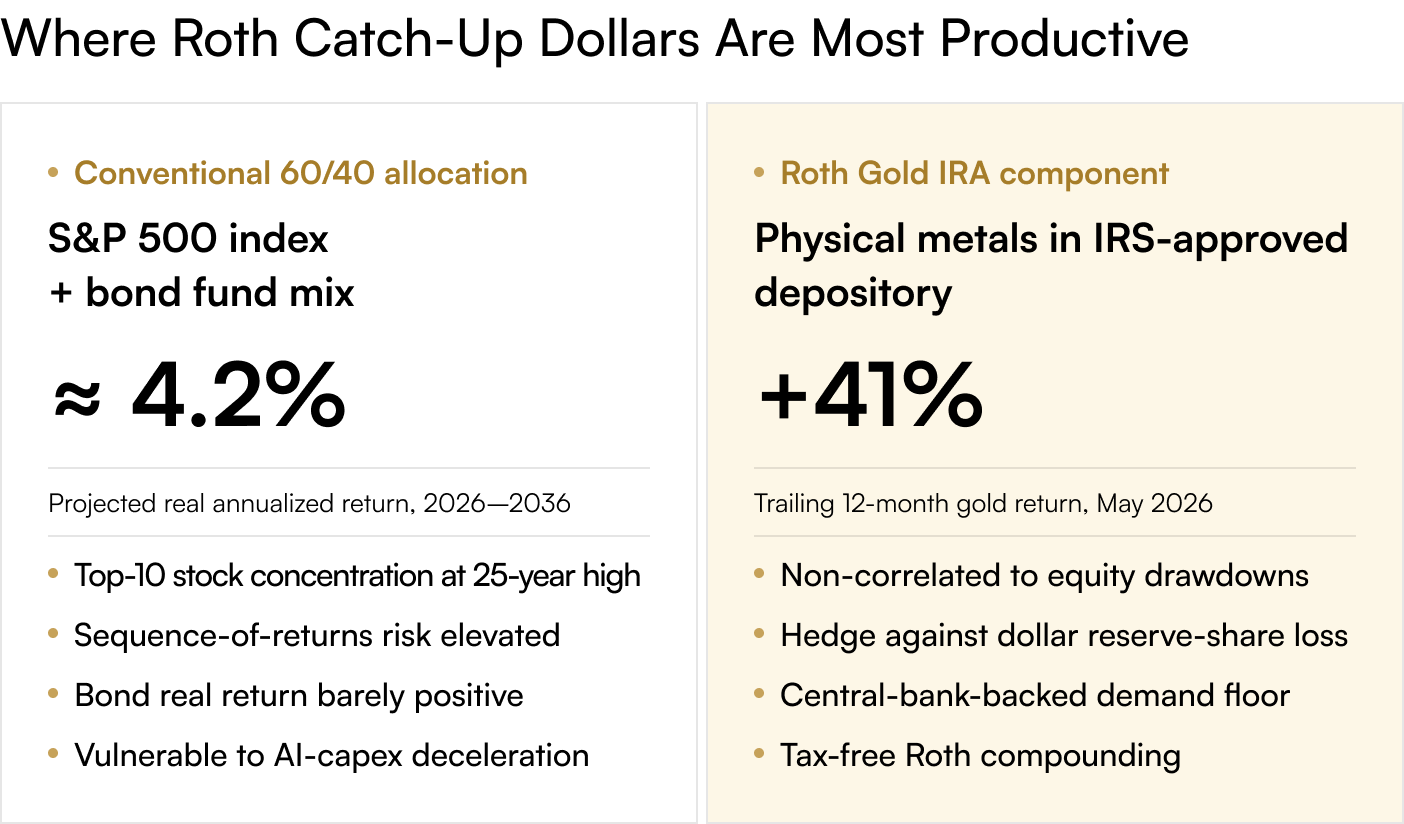

The Roth catch-up mandate is one of several signals that the federal government is moving aggressively to capture tax revenue earlier in the savings cycle. Other recent moves in the same direction include the elimination of the stretch IRA for non-spouse beneficiaries (covered in Article 4), the gradual upward push on RMD-age thresholds, and the introduction of new mandatory in-plan Roth options. Each of these changes makes Roth dollars relatively more valuable than they appeared in the prior decade — and savers paying ordinary-income rates today should be choosing Roth investments whose long-run real return is highest, because that is where the after-tax advantage compounds most aggressively.

Physical gold inside a self-directed Roth IRA fits the profile well. The metal's price appreciation is captured tax-free, and unlike a stock or bond, its long-run real return is not eroded by inflation, dividend taxation, or duration risk. The metal does not pay an annual dividend to be taxed at ordinary rates inside a taxable account; it simply appreciates against whatever monetary backdrop prevails. With gold up roughly 41% over the trailing year and Goldman Sachs, JPMorgan, TD Securities, and UBS converging on average 2026 forecasts of $5,400–$6,000, Roth dollars allocated to a precious-metals IRA in 2026 represent precisely the kind of long-duration, after-tax compounding the new rule was designed around.

The new Roth catch-up rule does not just change how high earners save — it changes what they should be saving into. Roth dollars are highest-value when invested in assets whose long-run real returns are large and durable. For 2026, that argues strongly for a precious-metals component inside the Roth structure. To determine whether a Roth-based Precious Metals IRA fits your 2026 contribution strategy and your existing tax picture, the team at Merchant Gold Group can perform a complimentary plan review and walk through the mechanics with you in plain language, including the rollover process and the IRS-approved storage options that govern these accounts.