175 basis points of Federal Reserve rate cuts since September 2024, the 10 year U.S. Treasury yield remains elevated at approximately 4.32% as of early April 2026. This disconnect between Fed policy and market yields reflects deepening concerns about fiscal sustainability, inflation persistence, and the credibility of long term monetary policy. For retirees and near retirees who have traditionally relied on Treasury bonds as the safe foundation of their portfolios, the current environment presents a toxic combination of reinvestment risk, duration risk, and purchasing power erosion that makes gold and precious metals an increasingly essential allocation.

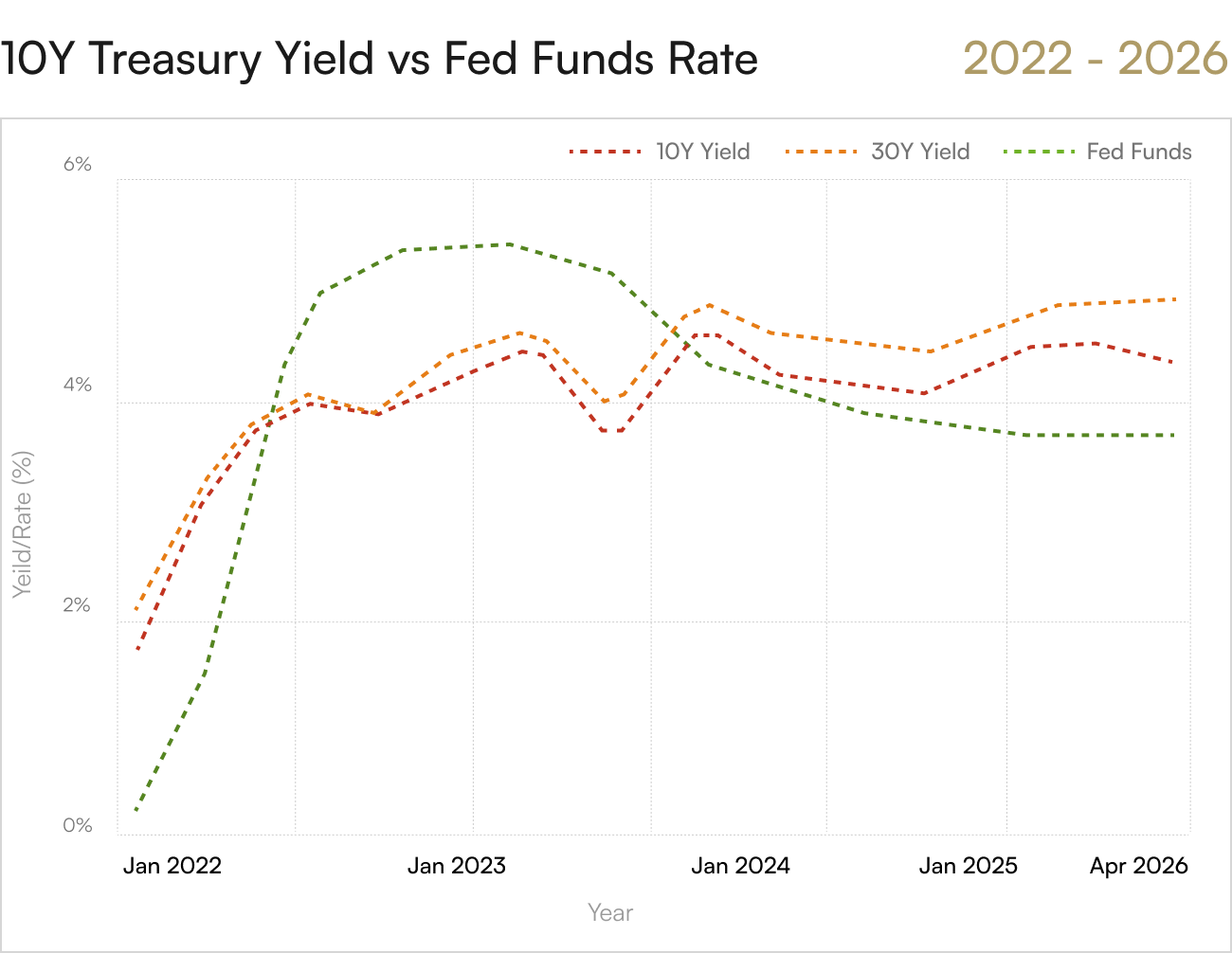

The Yield Curve Paradox

Normally, when the Federal Reserve cuts short term interest rates, longer term Treasury yields fall in anticipation of lower inflation and slower economic growth. That relationship has broken down in 2026. The Fed has lowered its benchmark rate from 5.25% to 5.50% down to 3.50% to 3.75%, yet the 10 year Treasury yield has remained stubbornly above 4%. The 2 year yield sits at 3.804%, and the 30 year yield trades near 4.913%. This persistent elevation in long term rates despite Fed accommodation signals that bond markets are pricing in structural risks beyond the central bank's immediate control.

Fiscal Deficits Are the Elephant in the Room

The United States is running massive fiscal deficits with no credible plan to reduce them. Higher long term interest rates reflect bond investors' demand for a risk premium to compensate for the uncertainty of lending to a government with deteriorating fiscal discipline. Term premiums, the extra yield investors demand for holding longer dated bonds instead of rolling over short term debt, have risen as markets price in fiscal stress. The federal government must continually refinance trillions in maturing debt at these elevated rates, creating a compounding interest burden that further worsens the deficit. This is a structural problem that the Fed cannot solve by cutting short term rates.

Inflation Is Not Going Away

The second reason long term yields remain elevated is inflation persistence. March 2026 CPI came in at 3.3% year over year, well above the Fed's 2% target. Energy prices surged 10.9% due to the Iran war, but core inflation also remains sticky in shelter, services, and goods. The Fed's own projections now expect 2.7% PCE inflation in 2026. Bond investors buying a 10 year Treasury at 4.32% are locking in a real yield of barely 1%, well below historical norms of 2% or more. If inflation stays elevated or reaccelerates, those bonds will deliver negative real returns for a decade.

The Bond Market Is No Longer Safe

For decades, retirement advisors preached the 60/40 portfolio: 60% stocks for growth, 40% bonds for safety and income. That framework is broken. Bonds are no longer a safe haven when yields fail to keep pace with inflation. The traditional inverse correlation between stocks and bonds has weakened, meaning bonds no longer provide effective diversification during equity drawdowns. And with the Fed politically pressured to keep rates lower than inflation justifies, bond investors face the very real risk that monetary policy accommodation will erode their purchasing power faster than coupon payments can compensate.

Gold Offers What Bonds No Longer Can

Gold does not pay a coupon, but it also does not carry credit risk, reinvestment risk, or duration risk. Gold cannot be debased by fiscal deficits or devalued by central bank printing. Gold has no maturity date and no counterparty. When inflation runs above nominal interest rates, gold preserves purchasing power while bonds destroy it. When fiscal credibility deteriorates, gold benefits from safe haven flows while bonds suffer from rising term premiums. When central banks are trapped between inflation and recession, gold thrives in the policy paralysis while bondholders suffer losses on both price and purchasing power.

.png)

Reallocate from Bonds to Precious Metals

Retirement investors holding long duration Treasury bonds yielding 4.32% in an environment of 3.3% inflation are accepting a real return of barely 1% while exposing themselves to significant interest rate risk and purchasing power erosion. That is not safety; that is slow motion wealth destruction. Physical gold and silver held in a self directed Precious Metals IRA offer an alternative that does not depend on government solvency, central bank credibility, or bond market liquidity. With gold trading near $4,700 per ounce and major institutions forecasting $5,400 to $6,000 by year end, the opportunity cost of holding underperforming bonds becomes clearer every day. Contact Merchant Gold Group today to learn how to reallocate a portion of your fixed income exposure into assets that actually preserve wealth rather than quietly erode it.