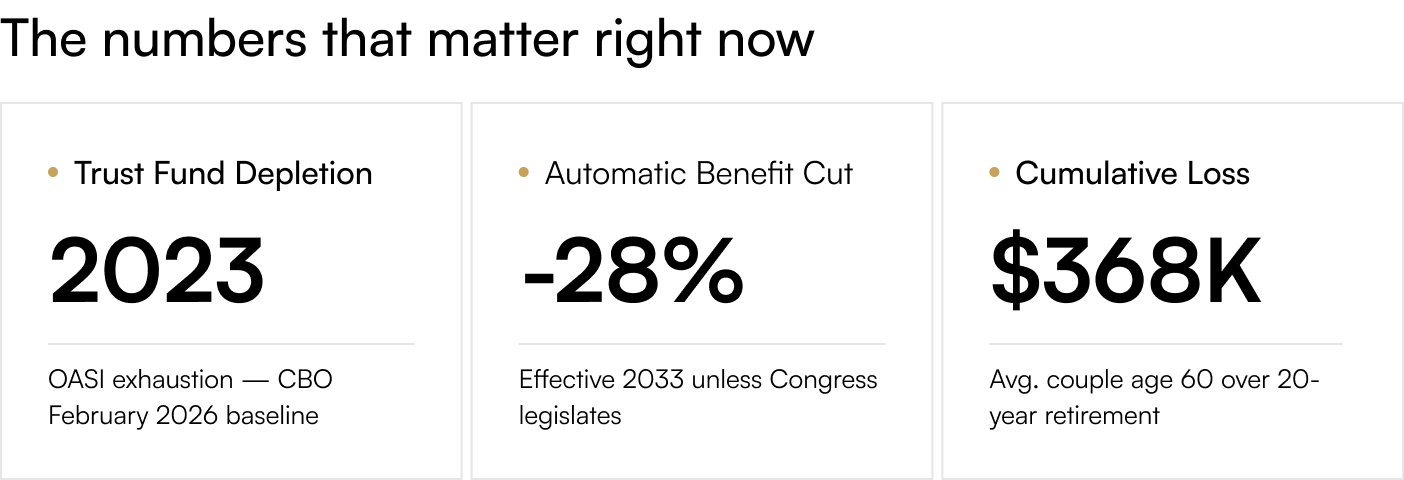

When the Congressional Budget Office released its updated baseline projections in February 2026, the headline figure was unambiguous and — for the roughly 70 million Americans currently receiving benefits — alarming. The Old-Age and Survivors Insurance (OASI) trust fund, the larger of the two reservoirs that fund Social Security, is now expected to be fully depleted in fiscal year 2032. That is one year sooner than the prior year's Trustees Report projected, and roughly five years sooner than the 2017 baseline that lawmakers were relying on when many of today's policy options were last seriously debated.

More importantly, the analysis quantifies the consequence of inaction. Once the trust fund is exhausted and Social Security must operate on payroll-tax inflows alone, benefits would be cut by approximately 28% across the board in 2033 — up from the prior 23% projection. For a typical couple aged 60 today, the Committee for a Responsible Federal Budget estimates an annualized benefit reduction of roughly $18,400 per year for the rest of their joint retirement. Over a 20-year horizon, that is more than $368,000 of cumulative income disappearing from a single household's retirement plan.

This is not a partisan talking point. It is the official baseline of the agency Congress relies on to score legislation.

ANATOMY OF THE PROBLEM

Why the Timeline Keeps Compressing

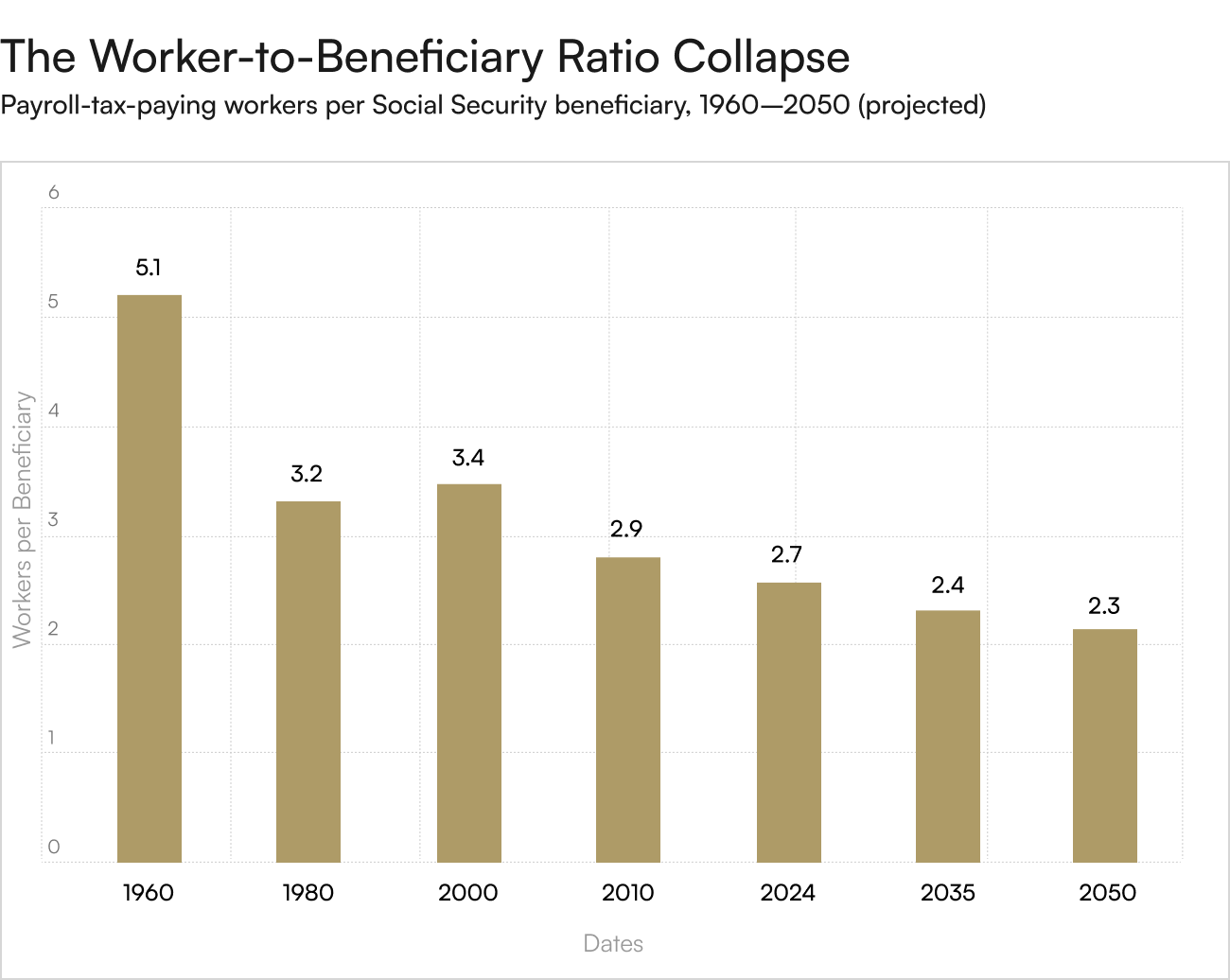

Social Security has faced funding shortfalls before. The most recent serious near-miss occurred in 1982, when the program came within months of being unable to pay full benefits. The Greenspan Commission resolved that crisis through a bipartisan package that raised the payroll-tax base, gradually increased the full retirement age, and brought new federal workers into the system. Critically, those reforms were enacted while the worker-to-beneficiary ratio was still favorable enough to make incremental adjustments effective. The 2026 environment is structurally different — and worse — on every meaningful dimension.

Three forces are compressing the runway. First, the 2025 Reconciliation Act created a new senior tax deduction that, while popular, reduces revenue flowing into the trust funds by an estimated tens of billions over the next decade. Second, net immigration — historically a structural positive for payroll-tax inflows — fell from roughly 2.8 million in 2024 to about 1.3 million in 2025, weakening the long-term ratio of contributing workers to benefit recipients. Third, the worker-to-beneficiary ratio itself has been collapsing for two generations, and the demographic math now leaves very little room for incremental fixes.

A Case Study in Misaligned Expectations

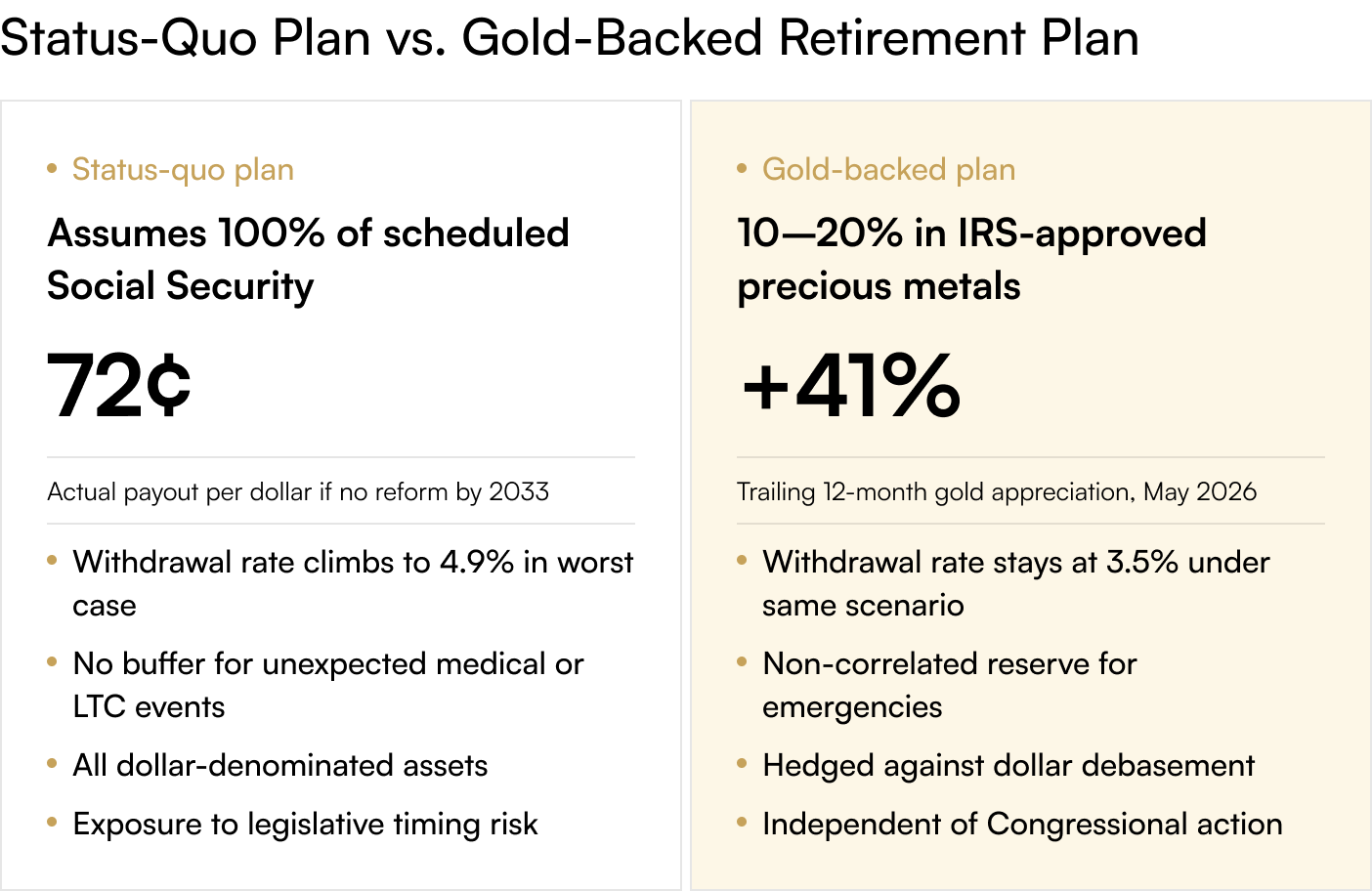

Consider the Hendersons, a hypothetical Ohio couple in their early sixties. Both worked full careers — he as a maintenance engineer, she as a public-school teacher with a small state pension. They planned conservatively. They paid off their home, saved diligently in 403(b) and 401(k) accounts, and budgeted for a retirement that would draw a meaningful share of monthly income — roughly 40% — from their combined Social Security checks beginning at full retirement age. Their plan, prepared by a fee-only adviser in 2022, assumed 100% of scheduled benefits. The plan worked on paper.

Under the new CBO baseline, if Congress does not act before 2033, the Hendersons will receive roughly 72 cents on the dollar of those promised benefits. Their portfolio's withdrawal rate jumps from a manageable 3.6% to a stressful 4.9%. Their margin for an unexpected medical event vanishes. Their two-week annual vacation becomes a four-day vacation. None of this is because they were imprudent. It is because the baseline they relied upon was, in retrospect, optimistic.

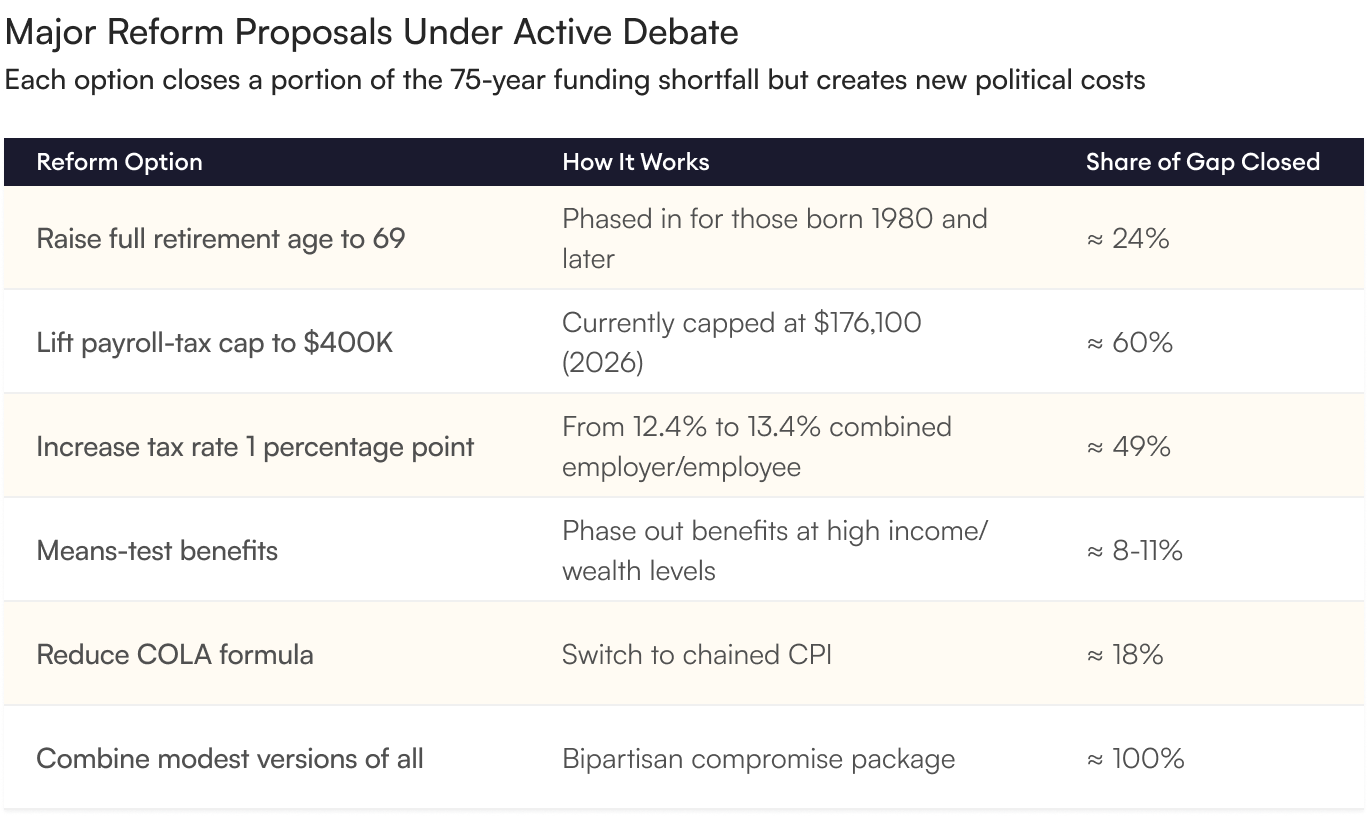

THE POLICY OPTIONS BEING DEBATED

Each Has a Cost — and Each Faces Stiff Resistance

Congress has, at various points over the past decade, floated several remedies. None has passed. The 2026 Congress has signaled it intends to engage the issue before the 2028 election cycle, but the political math is harder than the actuarial math. The table below summarizes the major options under discussion and their estimated impact.

Every one of these options reduces someone's promised benefit, raises someone's taxes, or both. The longer Congress waits, the more painful any single reform becomes. The 1983 fix could be enacted because it spread costs over decades and the demographic tailwind was forgiving. The 2032 fix, if it arrives at the last minute, will be steeper and more abrupt — which is precisely why households planning today cannot afford to assume legislators will deliver a clean rescue.

Why Physical Gold Enters the Conversation

Gold's role in this conversation is not to replace Social Security. It is to function as a parallel store of value whose performance is structurally independent of the U.S. payroll-tax base, the U.S. fertility rate, the immigration debate, the marginal voter in the House Ways and Means Committee, and every other political and demographic variable that determines what Congress eventually does with Social Security. That independence is, in the language of portfolio theory, an extremely valuable property.

Gold has functioned as monetary collateral across centuries of currency regimes, governmental reorganizations, and political crises. It is divisible, portable, non-counterparty, globally liquid, and — uniquely among major monetary metals — produced at a rate of only roughly 1.5% of above-ground stock per year, making rapid debasement effectively impossible. Central banks themselves understand this; they purchased a net 244 tonnes in Q1 2026 alone, and 95% of surveyed reserve managers indicated plans to increase their gold holdings further in 2026.

With gold trading near $4,700 per troy ounce in mid-May 2026 — a 41% year-over-year advance against a U.S. dollar that has lost reserve share to 54% — the metal has done precisely what an insurance asset is supposed to do: appreciate as confidence in the underlying architecture erodes.

The 2032 deadline is not a forecast or a worst-case scenario — it is the official baseline. Households that wait for Congress to act before adjusting their plans risk discovering that the political fix arrives later, smaller, and more expensive than expected. The most rational response is not to abandon Social Security planning but to add a parallel layer of protection that does not depend on it. To explore how a precious-metals allocation can sit alongside your existing retirement plan and protect against legislative drift, the team at Merchant Gold Group can walk you through a tailored Precious Metals IRA strategy and provide a complimentary copy of the firm's 2026 Retirement Defense Guide.

.jpg)