While senior gold producers like Newmont and Barrick offer steady leverage to rising gold prices, junior exploration companies provide explosive, asymmetric upside for investors willing to accept higher risk. At $4,700 per ounce gold, the economics of discovering a new deposit have transformed dramatically. A discovery that would have been marginally economic at $1,500 gold is now a Tier 1 asset. Projects that were shelved during lower price environments are being dusted off and re-evaluated. Junior explorers with the right geology, the right management teams, and the right jurisdictions are seeing their market capitalizations multiply 5x, 10x, or more when drill results hit. For retirement investors seeking diversification beyond large cap miners, and willing to allocate a small percentage of precious metals exposure to higher risk/higher reward opportunities, the junior exploration space offers leverage that cannot be matched anywhere else in the gold sector.

The Junior Explorer Business Model

Junior mining companies do not produce gold; they discover it. These are small cap exploration firms that acquire promising land packages, conduct geological surveys, drill exploratory holes, and attempt to delineate economic deposits that can eventually be sold to larger producers or developed into operating mines. The business model is binary: most exploration projects fail to find economic mineralization, but the ones that succeed can generate returns of 1,000% or more for early shareholders. Unlike senior producers whose stock prices move 2x to 3x with gold, successful junior explorers can move 10x, 20x, or 50x from discovery to resource definition to takeout by a major.

Why $4,700 Gold Changes Everything

At $1,500 gold, a deposit needs to be high grade, large tonnage, and in a favorable jurisdiction to justify development. At $4,700 gold, deposits that would have been uneconomic are now highly profitable. Projects with all in sustaining costs of $1,800 per ounce that were marginal at $2,000 gold now generate $2,900 per ounce margins. This expands the universe of economically viable projects and increases the valuation multiples that acquirers are willing to pay. Major producers sitting on stagnant reserves and facing declining mine life are desperate for new deposits. They cannot organically replace reserves fast enough through brownfield exploration. They must acquire juniors with proven resources. At $4,700 gold, they can afford to pay premium multiples because the acquired ounces are immediately accretive to their portfolios.

The Risk Profile

Junior explorers are not for everyone. The majority of exploration projects fail to find economic deposits. Management quality varies widely. Jurisdictional risk in unstable regions can destroy value overnight. Dilution from constant equity raises to fund drilling is common. Liquidity is poor in many micro cap names. Retail investors can lose 50%, 70%, or 100% of capital if a company burns through cash without making a discovery. This is high risk, high reward territory that requires diversification across multiple names, careful due diligence on management and geology, and position sizing that limits downside to 5% to 10% of total precious metals allocation. But for those willing to accept the volatility, the upside is unmatched.

What to Look For

Successful junior exploration investing requires identifying companies with proven management teams that have discovered and sold assets before, projects in tier one mining jurisdictions like Canada, Australia, Nevada, or certain Latin American countries with stable regulatory frameworks, geological settings that are known to host large deposits rather than one off anomalies, sufficient cash on the balance sheet to fund at least 12 to 18 months of drilling, and insider ownership that aligns management incentives with shareholders. Investors should also look for projects in districts where major producers already operate, as this increases the likelihood of an eventual takeout. Companies that publish technical reports compliant with NI 43-101 or JORC standards provide transparency on resource estimates and economics.

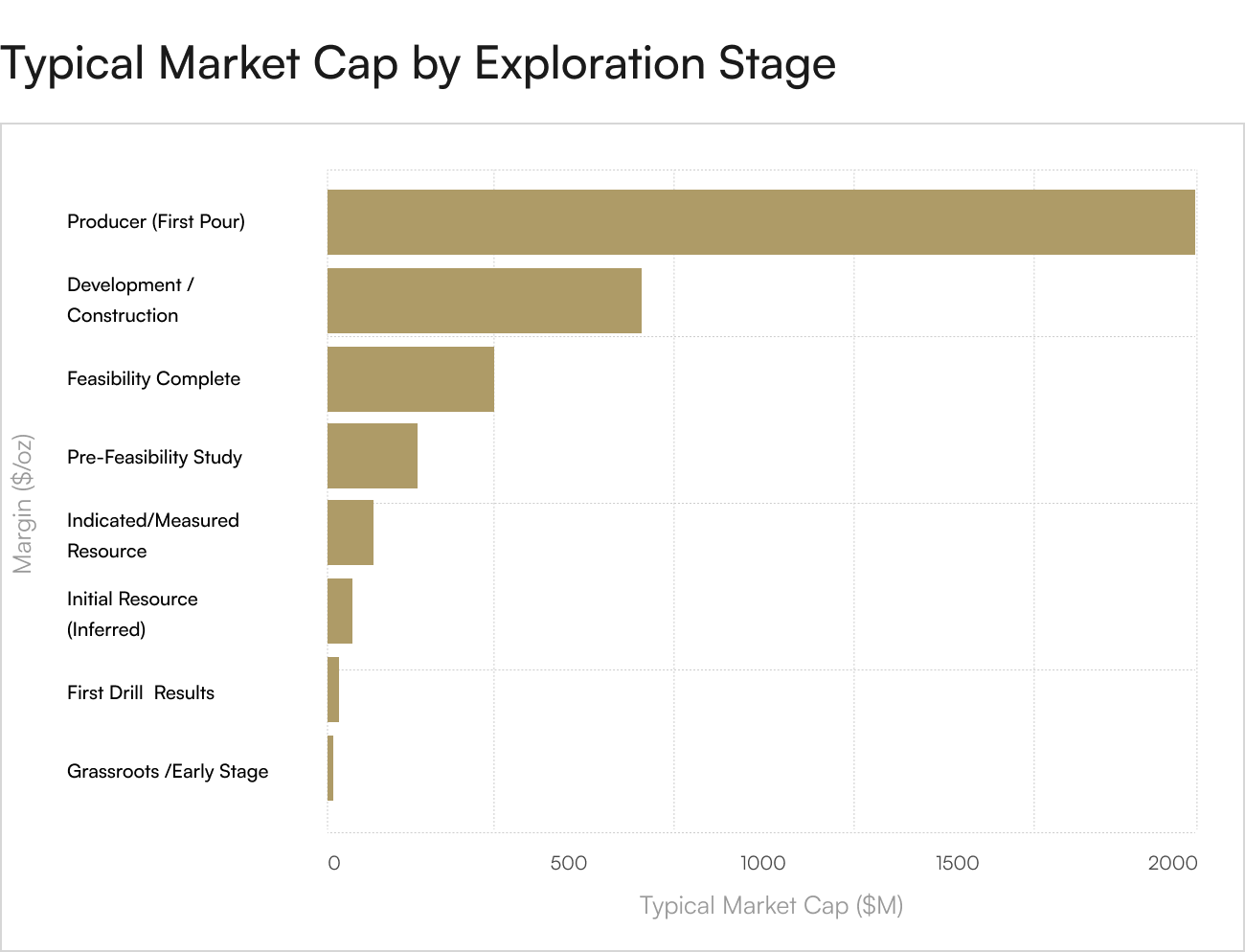

The Discovery Cycle

Junior exploration follows a predictable cycle. First, a company stakes claims or acquires a property. Second, it conducts surface sampling, geophysics, and initial reconnaissance to generate drill targets. Third, it raises capital to fund a drill program. Fourth, it drills and releases assay results. If results are positive, the stock spikes. If results are negative, the stock collapses. Successful companies move from discovery to resource definition, then to preliminary economic assessments, feasibility studies, and eventually permitting and construction or sale to a larger producer. Each stage creates re-rating opportunities. A company with a market cap of $20 million that discovers a 5 million ounce deposit could be worth $200 million or more after resource definition, and $500 million if a major offers a takeout premium.

A Small Allocation, Massive Upside

Retirement investors do not need to bet the farm on junior explorers. A 5% allocation to a diversified basket of 5 to 10 well selected juniors can provide asymmetric upside while limiting downside risk. If gold rises to $5,400 or $6,000 as Wall Street forecasts, and if even one or two of those junior positions delivers a 500% to 1,000% return from a successful discovery, the impact on total portfolio returns can be significant. This is not core holdings territory; it is the satellite allocation for investors who understand that the biggest gains in any bull market come from the small cap names that benefit most from rising commodity prices and whose valuations can re-rate violently on positive news.

Explore the High Octane End of Precious Metals

Junior gold exploration companies are not suitable for every investor, and they should never represent a majority of precious metals exposure. But for those with the risk tolerance, time horizon, and portfolio size to allocate a small percentage to this sector, the rewards can be life changing. At $4,700 gold and rising, the economics of discovery have never been better. Major producers have never been more desperate for reserves. And the leverage that successful juniors offer to rising gold prices is unmatched in the equity markets. Merchant Gold Group specializes in helping retirement investors construct diversified precious metals portfolios that balance the stability of physical bullion, the steady cash flow of senior miners, and the explosive upside of carefully selected junior explorers. Contact us today to learn how to capture the full spectrum of opportunities in a gold bull market that Wall Street's largest institutions believe is just getting started.