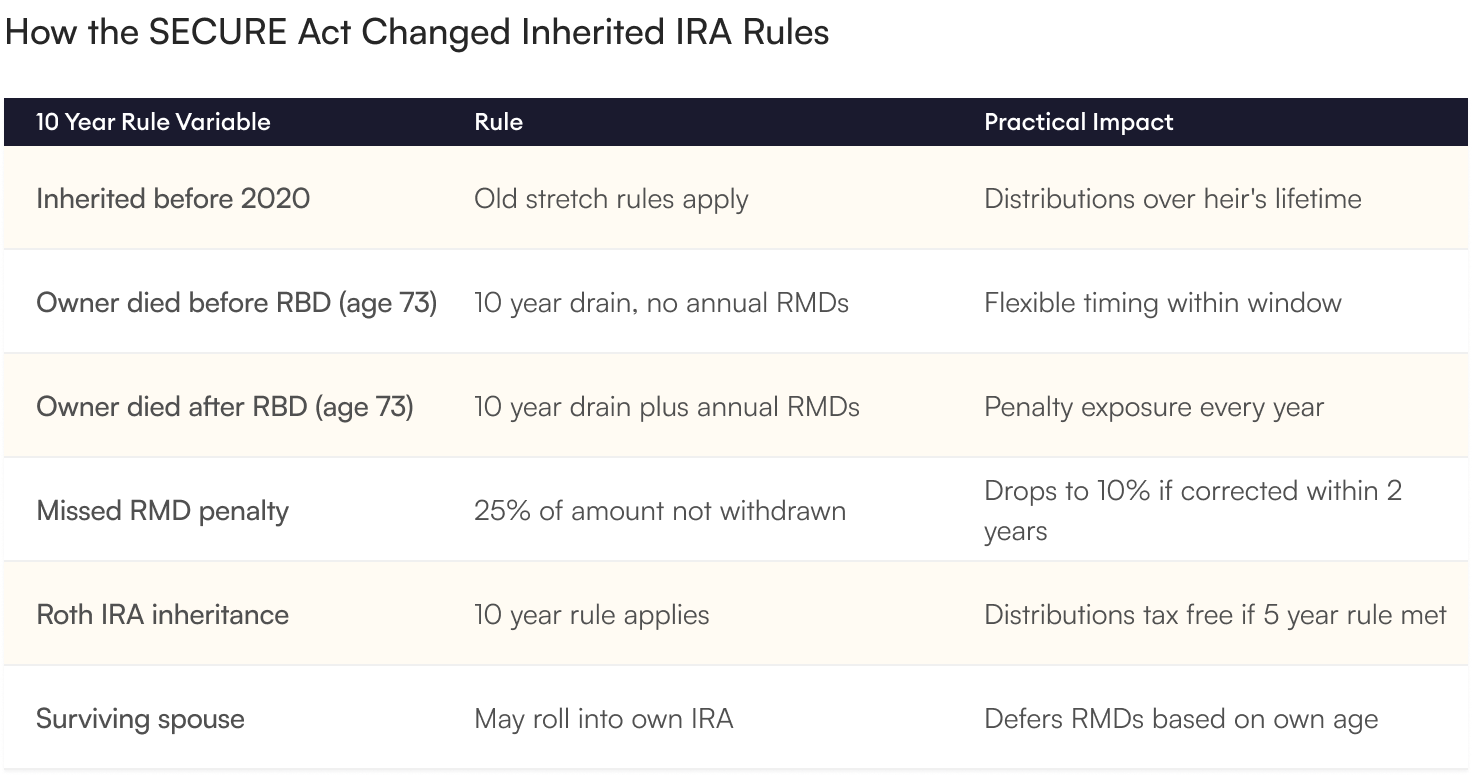

The IRA your client built over forty years is not the asset their children will receive. The Setting Every Community Up for Retirement Enhancement Act of 2019 quietly killed the stretch IRA, and SECURE 2.0 confirmed it. Most non spouse beneficiaries inheriting an IRA after December 31, 2019 must drain the entire account within ten years of the original owner's death. The IRS finalized the rules in 2024 in a way that made the trap considerably worse. If the original owner had already started Required Minimum Distributions, the heir must take annual RMDs inside that ten year window, with penalties starting at 25 percent of any missed distribution. For a six figure inheritance handed to a child already in their peak earning years, what used to be a 30 year tax deferred legacy becomes a 10 year forced liquidation that often pushes the heir into the next tax bracket.

Who Falls Under the 10 Year Rule

Most adult children, grandchildren, siblings, and unrelated beneficiaries fall under the 10 year rule. The exceptions are narrow and collectively known as Eligible Designated Beneficiaries. They include the surviving spouse, who has additional rollover options unavailable to other heirs, minor children of the deceased until they reach the age of majority, beneficiaries who are disabled or chronically ill under IRS definitions, and beneficiaries who are less than ten years younger than the decedent. Everyone else is subject to the ten year drain. Whether the heir must take annual RMDs inside that ten year window depends on a single fact, whether the original owner had reached their Required Beginning Date, currently age 73, before death.

The Hidden Tax Bomb

Consider a parent who passes away at age 78 with a $1.2 million traditional IRA. The non spouse adult heir, a 50 year old earning $180,000 per year, must drain the account within ten years and take annual RMDs along the way because the parent had already started distributions. If the heir spreads withdrawals evenly, that is roughly $120,000 per year of additional taxable income on top of their salary, pushing them firmly into the 32 percent federal bracket and possibly higher. State income tax, IRMAA surcharges if the heir is on Medicare, and reduced eligibility for various tax credits compound the damage. What looked like a generous inheritance becomes, in practical terms, a 35 to 45 percent forced tax event over a decade.

How a Roth Gold IRA Changes the Outcome

Converting traditional IRA assets to a Roth Gold IRA during the parent's lifetime transfers the tax burden away from the heir and back to the parent, who almost always pays at a lower marginal rate during the conversion window between retirement and age 73. The heir still has to drain the inherited Roth within ten years, but every dollar of that distribution is tax free. The parent has effectively prepaid the tax bill at their lower bracket and handed the heir an asset that produces no taxable distributions, no IRMAA exposure, and no bracket creep. Inside the Roth Gold IRA, physical gold can be distributed in kind to the heir, who takes physical possession of bullion, or sold for cash distributions depending on preference. The asset is exactly what was deposited, decades earlier, plus tax free appreciation.

Plan Now or Pay Later

Every retirement account owner with adult heirs has two questions to answer in 2026. First, has my beneficiary designation been reviewed since the SECURE Act passed in 2019. Second, would converting some portion of my traditional IRA to a Roth before death save my children meaningful tax. For most households the answer to the second question is yes, and the optimal strategy involves a multi year Roth conversion plan, often paired with a precious metals allocation that locks the inheritance into an asset class with no counterparty risk. Merchant Gold Group works with retirement and estate planning professionals on multi year conversion strategies, custodian transfers, and IRS approved depository storage. Contact our team today to ensure the inheritance you spent a lifetime building reaches your children intact, not eroded by a tax law most retirees did not see coming.