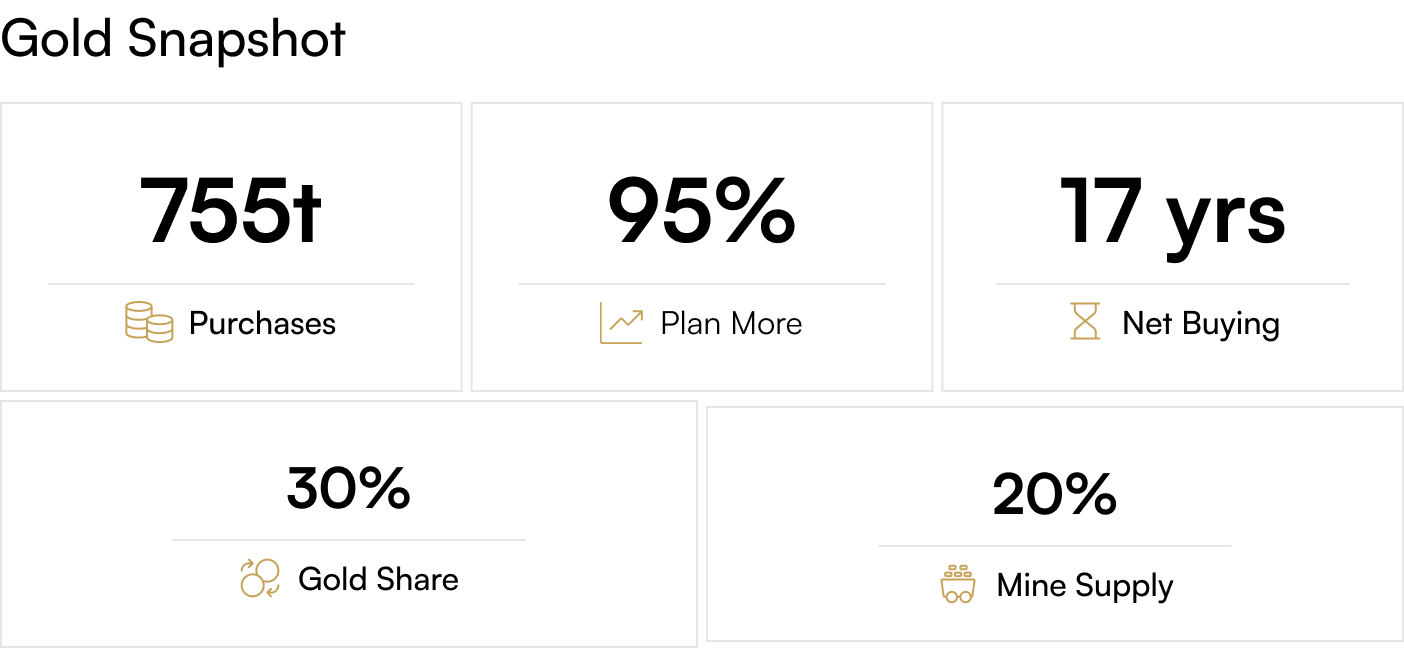

The world's central banks, the most sophisticated and well informed institutional investors on the planet, are telling you exactly where to put your money: gold. Projections for 2026 indicate central banks will purchase approximately 755 tonnes of gold, maintaining a multi year accumulation trend that has fundamentally reshaped the supply demand balance in the precious metals market. A World Gold Council survey found that 95% of central banks expect to increase their gold reserves in 2026, marking the 17th consecutive year of net official sector purchases since the Global Financial Crisis. This is not market timing or speculative momentum; this is the calculated reallocation of sovereign wealth away from fiat currencies and into the only asset with no counterparty risk, no political risk, and no debasement risk.

Record Breaking Accumulation

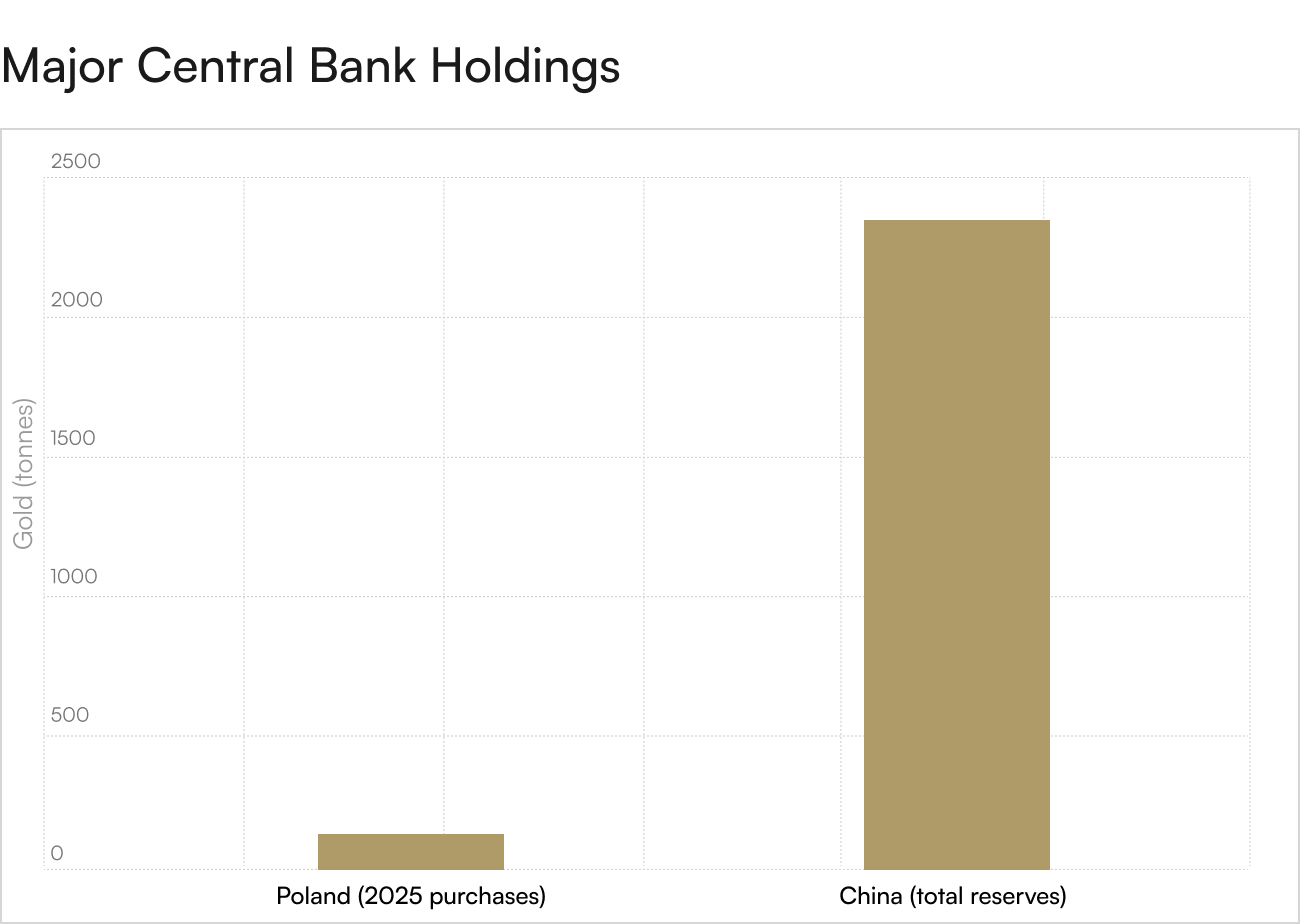

Central banks purchased approximately 863 tonnes of gold in 2025, marking the third consecutive year of purchases exceeding 1,000 tonnes when unreported buying is included. The actual figures for 2022 were 1,082 tonnes, for 2023 were 1,037 tonnes, and for 2024 were 1,045 tonnes. The World Gold Council projects 750 to 850 tonnes of central bank purchases in 2026, equivalent to roughly 26% of total annual mine output. Poland emerged as the largest reported buyer in 2025, acquiring 80 to 95 tonnes with an explicit target of holding 20% of national reserves in gold. China's People's Bank extended its gold buying streak to 16 consecutive months through late 2025, with reserves reaching 2,309 tonnes representing 10% of total foreign exchange holdings.

Why Central Banks Are Buying

Central banks accumulate gold for structural, strategic reasons that have nothing to do with short term price speculation. First, gold provides diversification away from fiat currency reserves that carry counterparty and credit risk. Second, gold cannot be frozen, sanctioned, or weaponized, making it the ultimate sovereign asset in an era of geopolitical fragmentation. Third, gold acts as an inflation hedge and store of value during periods of currency debasement. Fourth, regulatory changes under Basel III allow banks to hold gold with zero risk weighting on their balance sheets, upgrading gold to a Tier 1 asset equivalent to cash. Fifth, as the dollar's reserve share declines from 73% in 2001 to 54% in 2025, central banks are rebalancing portfolios toward assets that are not subject to any single nation's monetary policy.

The Supply Deficit This Creates

Global gold mine production is approximately 3,000 tonnes per year. If central banks are purchasing 755 tonnes, they are absorbing 25% of annual mine supply before a single ounce reaches jewelry, industrial, or private investment demand. This creates a structural supply deficit that puts upward pressure on prices. Goldman Sachs raised its year end 2026 gold price target to $5,400 per ounce, citing central bank purchases forecast at 60 tonnes per month as a primary driver. JPMorgan projects gold pushing toward $5,000 per ounce by Q4 2026, with $6,000 a possibility longer term. These are not speculative price calls; they are mathematical projections based on 585 tonnes per quarter of combined investor and central bank demand.

Emerging Markets Lead the Charge

The geographic distribution of central bank gold buying has shifted decisively toward emerging markets. Poland, Turkey, India, China, and other developing nations are the marginal buyers, while Western central banks have been largely inactive or even net sellers in some years. This reflects a fundamental realignment of global monetary power. Emerging market central banks witnessed the weaponization of dollar reserves against Russia and concluded that holding Western fiat currencies creates unacceptable political risk. They are diversifying into gold not as a short term trade but as a permanent structural shift in reserve allocation. Uzbekistan was the largest buyer in January 2026, while countries like Malaysia and South Korea that had been inactive for years resumed increasing their gold reserves.

Follow the Smart Money

When 95% of the world's central banks, institutions with access to the best economic research, the most sophisticated risk models, and the deepest market intelligence, are all making the same portfolio decision to increase gold allocations, retail investors should pay attention. Central banks do not chase momentum. They do not trade on sentiment. They allocate capital based on decades long strategic considerations about preserving sovereign wealth. Their consensus view is unmistakable: gold is undervalued relative to the risks in the fiat monetary system, and current price levels represent an opportunity to accumulate before structural supply deficits and currency debasement drive prices significantly higher.

Position Alongside the World's Central Banks

Retirement investors face a choice: align their portfolios with the institutions managing trillions in sovereign reserves, or bet against them. Central banks projecting 755 tonnes of gold purchases in 2026 while 95% plan to increase reserves are sending a clear signal about the future of monetary wealth. Physical gold and silver held in a self directed Precious Metals IRA allow individual investors to replicate the strategy of the world's most informed institutional buyers. You are not speculating on gold; you are following the largest and most patient capital allocators in the world into an asset they have determined is essential for long term wealth preservation. Contact Merchant Gold Group today to learn how to position your retirement portfolio in alignment with the global central banking community's consensus view that gold is the ultimate monetary asset for the decade ahead.