Central banks bought a net 244 tonnes of gold in the first quarter of 2026 — a three percent year-over-year increase, even with the metal trading at multi-record highs. That figure, published by the World Gold Council in its Q1 2026 Gold Demand Trends report, marks the continuation of a buying pattern that has now run for more than three years and shows no sign of breaking.

For retail and high-net-worth investors, the question is no longer whether central banks are repositioning their reserves. The question is what their behavior signals about the next decade of monetary policy and currency risk — and whether private balance sheets ought to mirror, in miniature, what sovereign balance sheets are doing in size.

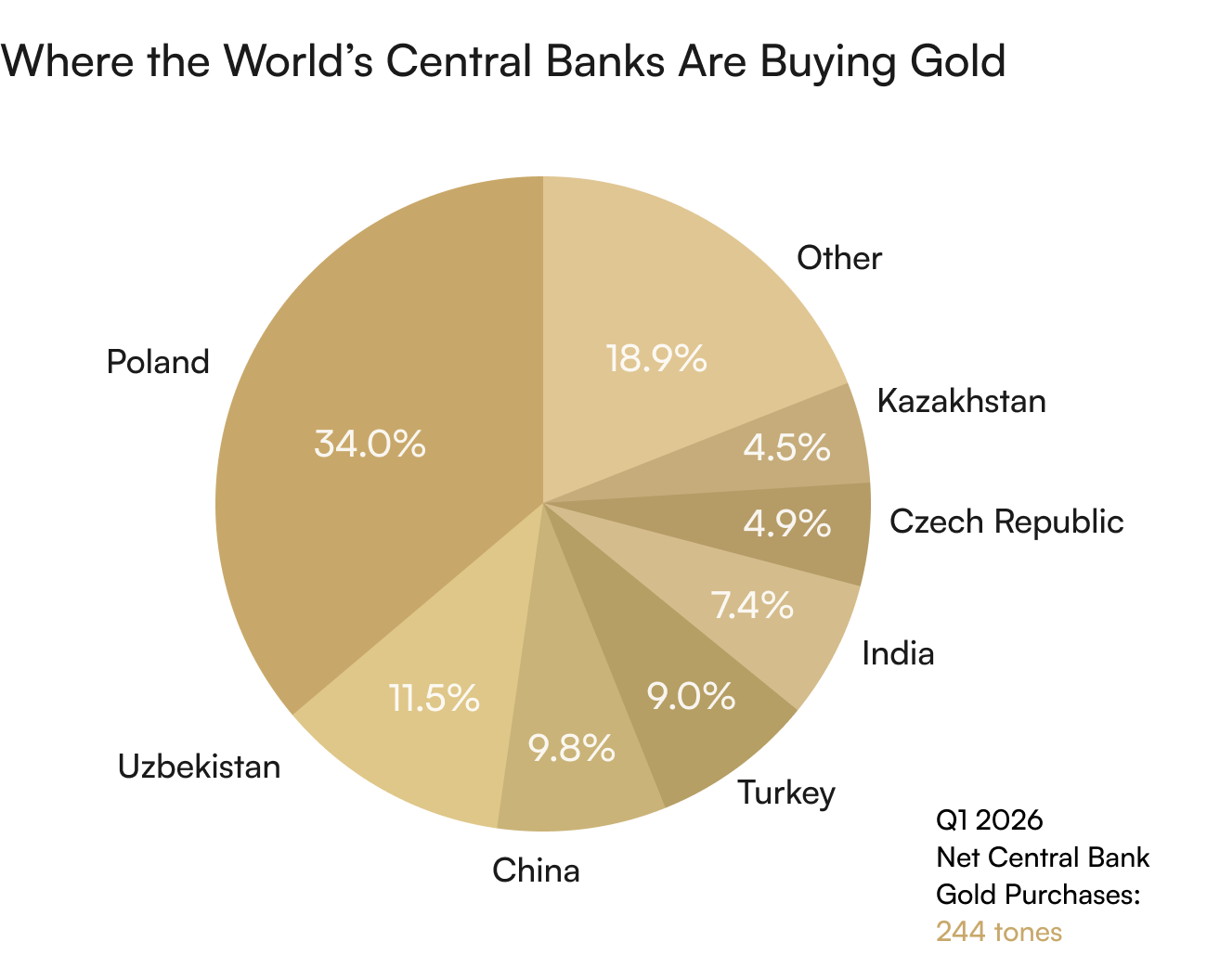

Who Is Actually Buying

The leaderboard for early 2026 looks very different from a decade ago. Poland has been the standout, leading global gold accumulation as part of a multi-year program targeting 700 tonnes of total reserves. Uzbekistan and Kazakhstan continue their steady Central Asian accumulation. The People's Bank of China extended its multi-month buying streak, even as published volumes remain modest relative to the country's overall reserve size. Turkey, after monetizing significant gold tonnage in 2025 to manage domestic financial pressures, has resumed buying.

On the other side of the ledger, a small group of central banks did sell during the quarter — typically because of liquidity needs, currency pressures, or active rebalancing. The World Gold Council notes that net buying remains the dominant trend, with 95 percent of central banks surveyed expecting global gold reserves to grow over the next twelve months.

Why Sovereign Buyers Care About Gold

Central banks accumulate gold for reasons that have very little to do with short-term price speculation. Reserve managers are tasked with preserving purchasing power across decades, diversifying away from any single counterparty, and holding assets that perform during the precise scenarios that damage other reserve instruments — sanctions, currency crises, sovereign defaults, and geopolitical shocks.

The 2022 freezing of approximately $300 billion in Russian central bank assets accelerated this thinking dramatically. For any country whose reserves sit primarily in U.S. dollars or euros, the lesson was unambiguous: financial assets held in another country's banking system can be unilaterally restricted. Physical gold held in domestic vaults cannot.

“The shift from dollar reserves to gold is not a prediction at this point — it is a multi-year trend driven by reserve managers acting on durable, structural risks.” — Gold market commentary, Q1 2026

What This Means for Private Investors

Sovereign buying matters for two reasons. First, it provides a structural floor under gold demand. J.P. Morgan models roughly 800 tonnes of central bank gold purchases in 2026, and even a meaningful step-down from prior years would still leave demand well above the pre-2022 average of 400 to 500 tonnes annually. That floor mechanically supports prices regardless of investor sentiment in any given quarter.

Second, central bank behavior often anticipates risks that retail and institutional investors only address later. The same logic that motivates a reserve manager to add gold — concern about debt sustainability, currency debasement, geopolitical fragmentation, and the resilience of the existing monetary order — also applies, scaled down, to a household balance sheet. A retiree relying on dollar-denominated bonds and equities is exposed, in a smaller way, to the same forces a sovereign reserve fund tries to insure against.

Mirroring the Logic, Not the Size

A private investor will never hold tonnes of gold. But the principle of allocating a modest, diversifying portion of one's net worth into a non-yielding hard asset that performs uncorrelated to bonds and equities during stress periods is the same principle a reserve manager applies. Most institutional allocation models suggest five to fifteen percent in physical precious metals, depending on risk tolerance and time horizon.

That allocation can take many forms — sovereign coins, bullion bars, or a self-directed precious-metals IRA. The common thread is physical ownership, with the metal held by a credible custodian rather than represented by a paper claim that depends on a counterparty's solvency.

Lessons Learned

When the world's most conservative financial institutions add gold quarter after quarter at all-time-high prices, that is a signal worth reading carefully. For a clear, no-pressure conversation about how a measured physical-gold position can be added to your retirement account or personal holdings, connect with a Merchant Gold Group specialist directly and review the same IRS-approved coins and bars that anchor sovereign reserve programs around the world.