The U.S. dollar is not being replaced as the world's reserve currency. It is, however, being slowly diluted as the dominant component of how countries hold their savings — and the data on that dilution has become impossible to ignore for anyone trying to understand where global capital is moving in 2026.

This is not a story about the dollar collapsing. It is a story about composition. And it has direct implications for any saver whose retirement is denominated in the currency that is, very quietly, losing reserve share for reasons unlikely to reverse.

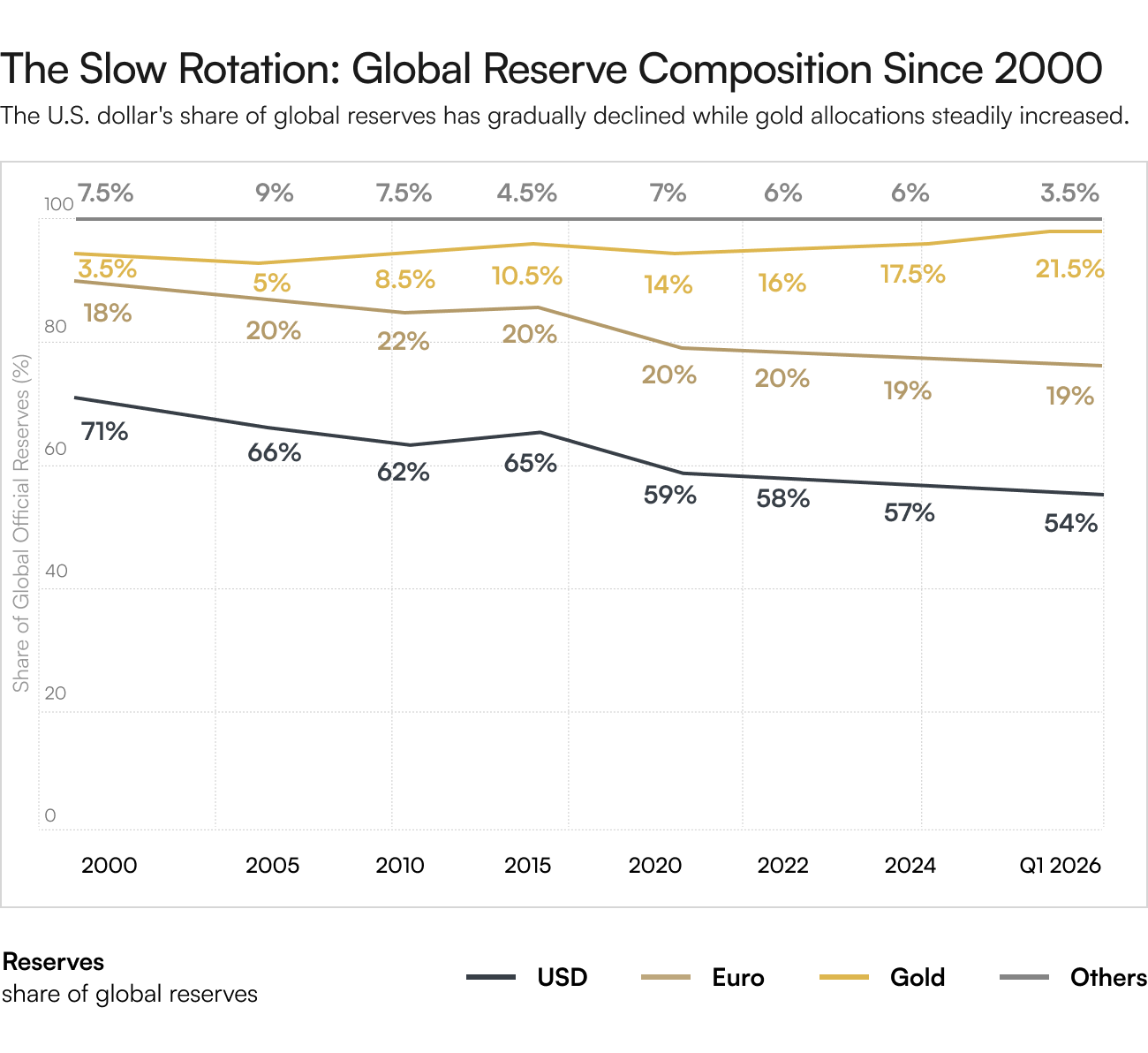

The Numbers Behind the Headlines

According to the International Monetary Fund's COFER database, the dollar's share of allocated global foreign exchange reserves has fallen from over seventy percent in 2000 to roughly fifty-six percent by early 2026. That is not a panic-grade decline, but it is a clear multi-decade trend. Over the same window, gold's share of total official reserves has moved from roughly three to four percent into the high teens or low twenties, depending on how the metal's market value is measured.

The euro has not absorbed most of the dollar's lost share. The Chinese yuan has gained marginally. The biggest beneficiary, in percentage-share terms, has been gold itself — and the marginal buyers driving that shift are concentrated in a specific set of countries: BRICS members, BRICS+ partners, and central Asian economies, with a few European holdouts like Poland adding aggressively for security-related reasons.

Why the Composition Is Shifting

Three structural drivers explain most of the rotation, and none of them is likely to fade quickly. The first is the 2022 freezing of approximately three hundred billion dollars in Russian central bank assets, which made unmistakably clear to every non-aligned reserve manager that financial assets held in another country's banking system are subject to that country's politics. Gold held in domestic vaults is not.

The second is the simple weight of U.S. fiscal arithmetic. Reserve managers tasked with preserving real value over decades cannot ignore a creditor whose debt-to-GDP ratio is rising on a structurally unsustainable trajectory, even if the near-term outcome is benign. Gold is the only large-scale reserve asset that is no one's liability.

The third is the slow construction of alternative payments infrastructure — settlement systems, bilateral currency arrangements, and reserve-pooling mechanisms among BRICS+ economies. None of these displaces the dollar in any meaningful sense, but together they reduce the marginal demand for dollar reserves to facilitate cross-border activity.

“The shift from dollar reserves to gold is not a prediction; at this point it is a measurable trend that has been running for over a decade and is broadening to a wider group of central banks.” — Reserve management research, 2026

What This Means for U.S.-Based Savers

A long-term, gradual rebalancing of global reserves out of the dollar and into gold and other instruments has two practical effects on a U.S. household. First, it provides structural support for the gold price independent of any short-term Federal Reserve decision or market sentiment cycle. The buyers driving the trend are constrained, methodical, and price-insensitive in the way that only sovereign reserve managers can be. Second, it gradually reduces the real purchasing power of dollar-denominated savings as the currency's share of global demand erodes at the margin.

Neither effect is dramatic on a one-year view. Both are meaningful on a ten- or twenty-year view, which is precisely the relevant horizon for retirement planning. For households whose entire savings base is denominated in the currency losing reserve share, owning a measured allocation to the asset gaining that share is one of the more direct hedges available.

Why Physical, Not Paper

The reason central banks add physical gold rather than paper exposure is not philosophical. It is practical: physical gold held in the country's own vault has no counterparty, cannot be frozen, and continues to function during any of the scenarios that damage other reserve assets. Households holding gold for the same reasons benefit from the same wrapper. A precious-metals IRA holding bullion at an IRS-approved depository, or coins held personally, accomplishes structurally what a sovereign vault accomplishes for a country.

Paper gold offers the price exposure but reintroduces the financial-system dependency that the asset was added to remove. For a hedge to work as intended, the wrapper has to match the thesis.

The Bottom Line for Investors. The reserve rotation is one of the slowest, most durable trends in global finance, and it is one of the few that is unambiguously visible in published central bank data. If you would like to understand how a measured physical-gold and silver allocation could fit alongside your existing retirement and brokerage portfolio, connect with a Merchant Gold Group specialist — the conversation is straightforward, the products are transparently priced, and the decision is yours.