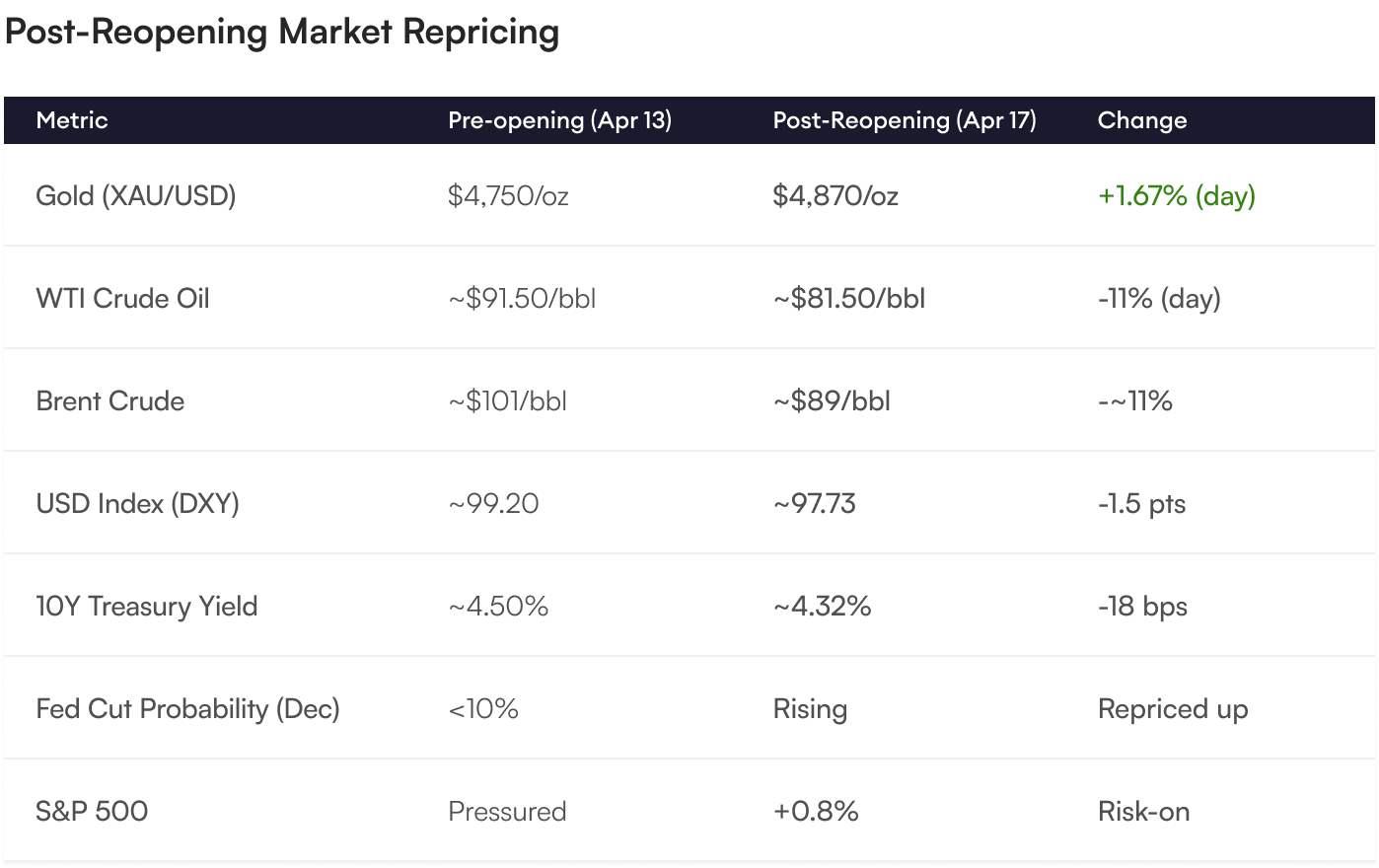

Iranian Foreign Minister Abbas Araghchi announced this morning that the Strait of Hormuz is declared completely open to all commercial vessels for the duration of the ceasefire in Lebanon. The announcement triggered an immediate 11% collapse in oil prices, sent the U.S. Dollar Index to one-month lows, and — critically for precious metals investors — pushed gold above $4,870 per ounce, up 1.67% on the day and on track for a fourth consecutive weekly gain.

This is not simply an energy story. The Hormuz reopening is a complex, multi-layered geopolitical reset that creates a decisive new investment environment. Understanding exactly what it means, what it does NOT resolve, and how to position your retirement portfolio before the next chapter unfolds is the purpose of this report.

The 49-Day Crisis in Context

On February 28, 2026, coordinated U.S. and Israeli airstrikes on Iran triggered a cascade of consequences that reshaped global energy and financial markets within hours. Iran's immediate response was to close the Strait of Hormuz, the 21-nautical-mile bottleneck through which approximately 20 million barrels of oil per day flow, representing roughly 20% of global seaborne oil and 20% of global liquefied natural gas trade. The International Energy Agency called the disruption the largest supply shock in the history of the global oil market.

Over the following seven weeks, WTI crude surged from below $75 to above $103 per barrel. Energy-driven inflation pushed March 2026 CPI to 3.3% year over year, with the energy component alone registering a 10.9% year-over-year spike. The Federal Reserve, which had been signaling rate cuts, was forced into an extended pause. The geopolitical risk premium was injected into every asset class on the planet.

What the Market Did Today — And What It Means

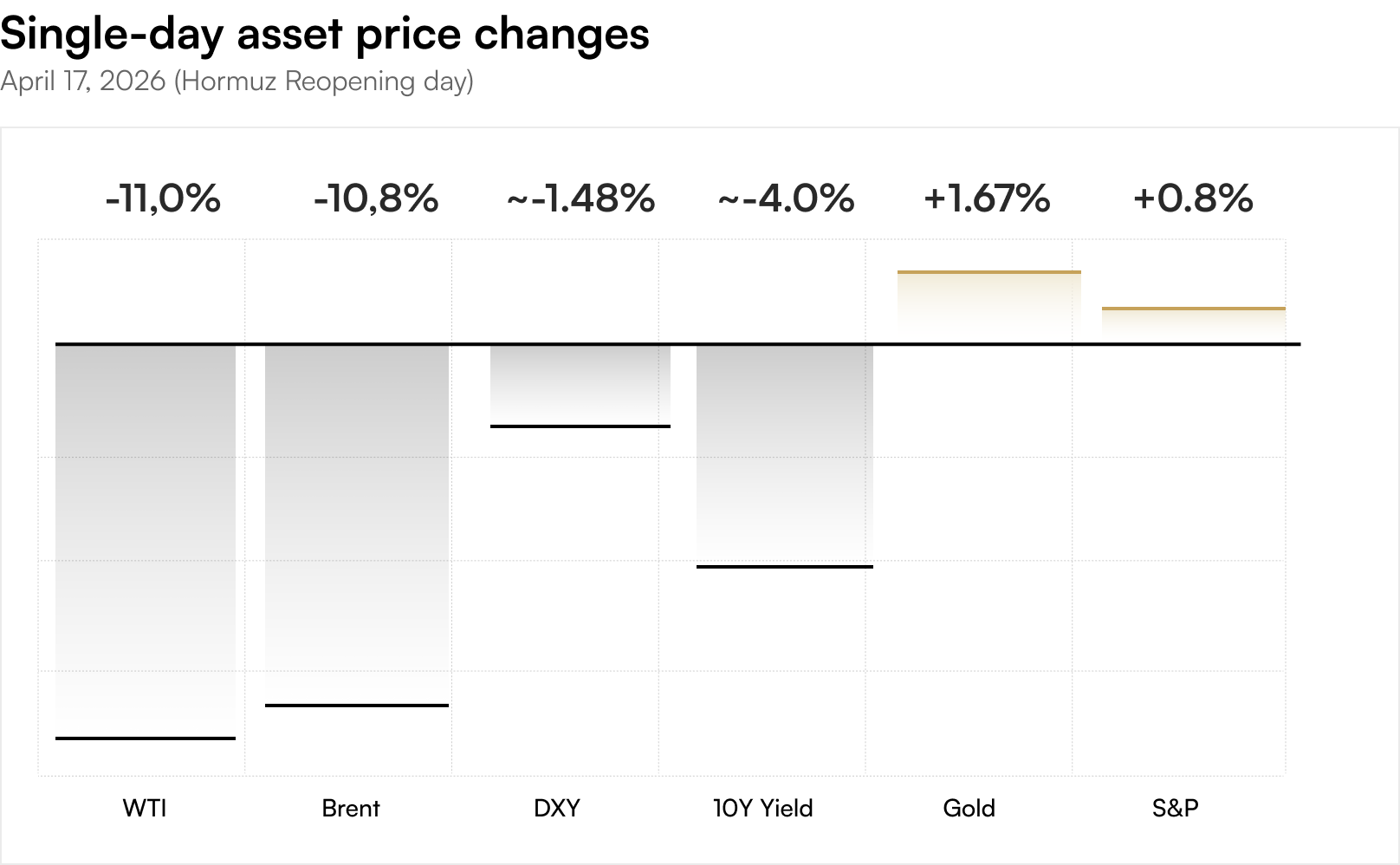

The market reaction to Iran's reopening announcement was swift, decisive, and instructive. Oil prices fell more than 11% intraday, the sharpest single-day collapse in crude in months. The dollar weakened, bond yields fell, Fed rate cut expectations were immediately repriced higher, and equity markets rallied. Gold, rather than falling on the perceived reduction in geopolitical risk, rose.

Gold rose because the reopening does not resolve the deeper monetary conditions that have been driving its multi-year bull market. Lower oil prices ease near-term inflation, which creates room for Fed rate cuts, and falling real interest rates are one of gold's most reliable tailwinds. The market is correctly interpreting the Hormuz reopening as bullish for gold through the monetary policy channel even as the geopolitical risk premium partially unwinds.

Why Gold Rose When Oil Fell — The Policy Channel

The conventional narrative says gold and oil move together in geopolitical crises because both benefit from fear and uncertainty. That relationship is real but incomplete. Gold has deeper, more durable drivers that are actually reinforced by lower oil prices in the current environment.

The Rate Cut Reinstatement Effect

Before the Hormuz closure, markets had priced roughly one Federal Reserve rate cut for 2026 and were growing increasingly skeptical that even one would materialize. The closure of the strait, and the 10.9% energy inflation it caused, all but eliminated any near-term rate cut probability. The CME FedWatch tool was showing a 99.5% probability of a hold at the April 28-29 FOMC meeting. That is the worst possible environment for gold: high inflation that keeps rates elevated, a hawkish Fed, and rising real yields.

Today's Hormuz reopening changes that calculus immediately. A sustained drop in oil prices can subtract 0.5% to 1.0% from headline CPI within two to three months. If WTI stabilizes at $80-85 rather than $100-110, the Fed gains room to act. Fed Governor Christopher Waller acknowledged directly today that the oil price decline could pave the way to rate cuts later in 2026. Every basis point of expected rate cuts is a tailwind for non-yielding gold.

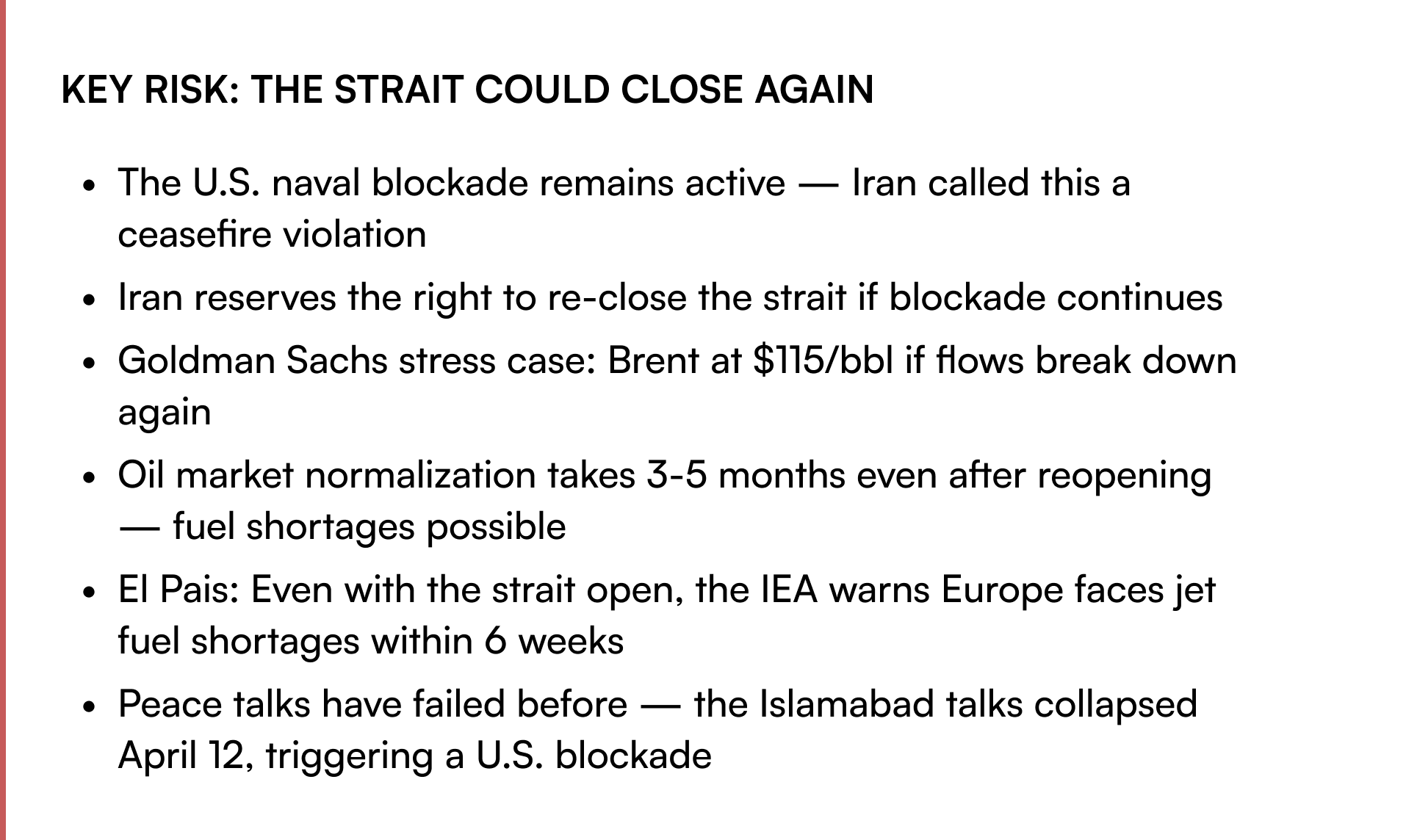

The Ceasefire Is Conditional — Not a Resolution

This is perhaps the most important strategic insight for investors to absorb: the Strait of Hormuz is open for the duration of the ceasefire in Lebanon, not permanently. Iran has explicitly retained the right to re-close the strait. The U.S. naval blockade remains in place pending a final agreement. Goldman Sachs, while cutting Q2 oil forecasts, explicitly maintained a stress case of $115/bbl Brent if the Middle East situation breaks down again.

The ceasefire architecture is fragile by design. It depends on the Lebanon truce holding, on U.S.-Iran negotiations progressing, on Iran not exercising its stated right to close the strait if the U.S. blockade continues. Analysts cited by CNBC described gold as remaining highly sensitive to political developments in the near term — a conditional ceasefire is precisely the kind of environment where gold maintains a structural bid even as the headline risk premium partially deflates.

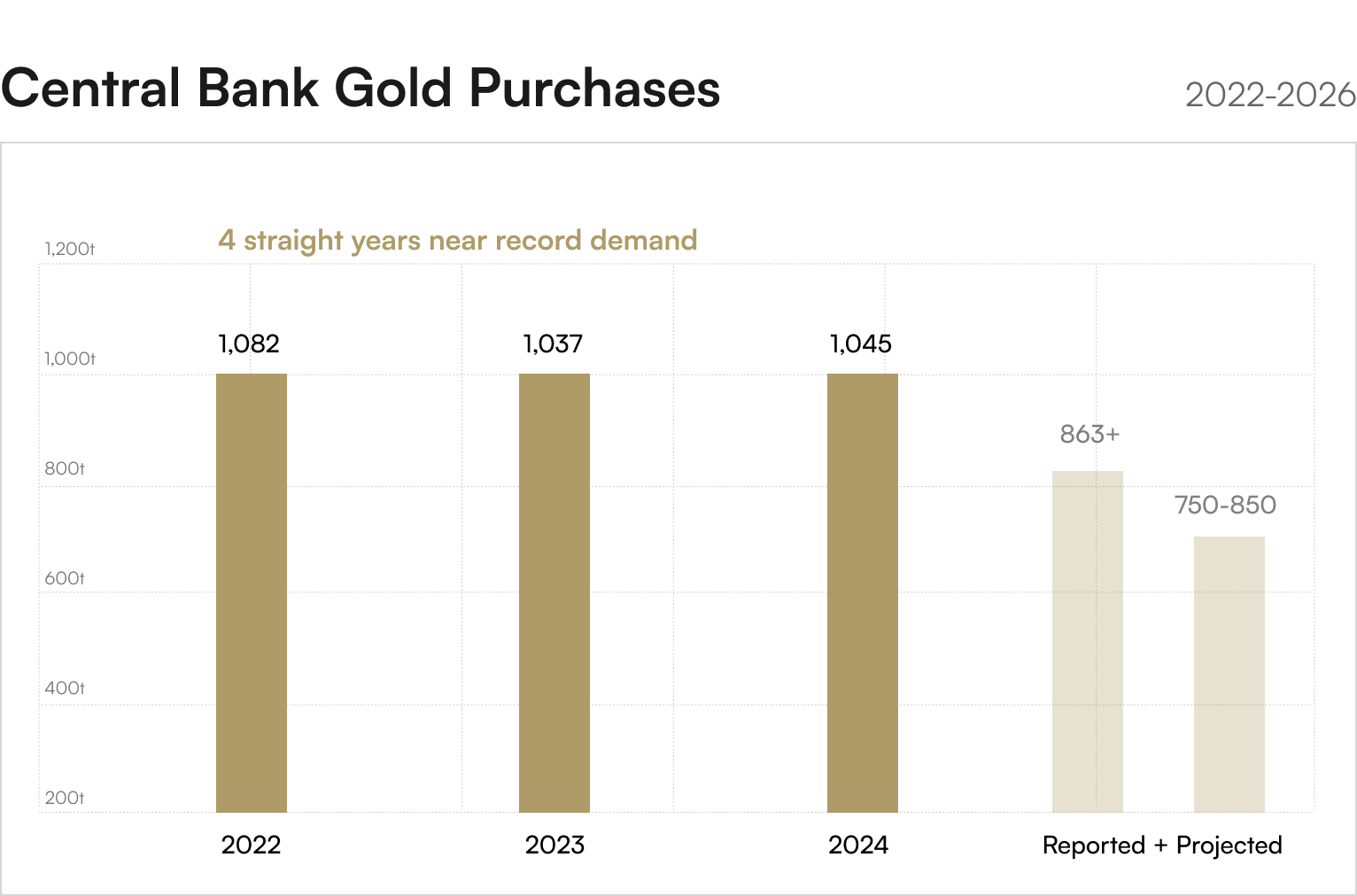

The Supply Deficit No One Is Talking About

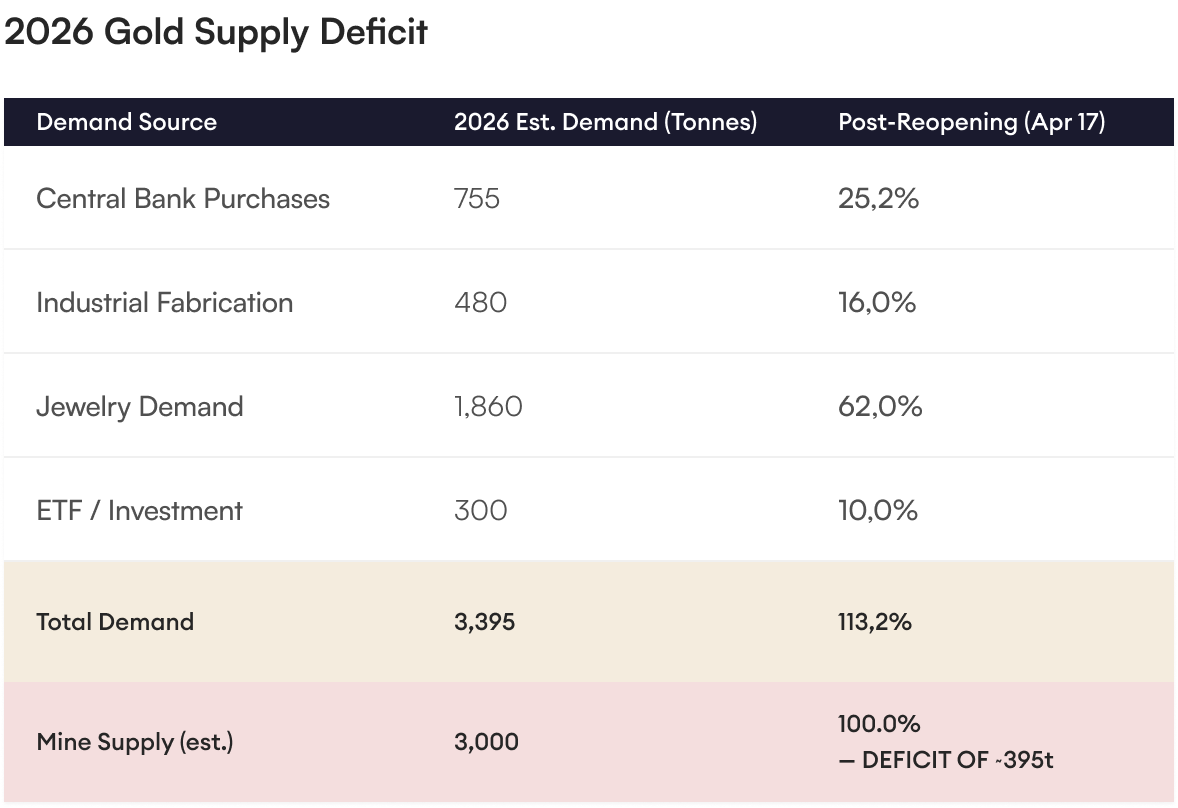

Lost in the noise of oil prices and geopolitical headlines is a gold-specific supply crisis that exists independently of any Middle East developments. The World Gold Council's 2026 data and projections from J.P. Morgan and Goldman Sachs collectively paint a picture of structural supply insufficiency that makes the case for gold ownership compelling regardless of whether the Hormuz ceasefire holds.

Central banks alone are projected to purchase 755 tonnes of gold in 2026, representing 25% of annual mine supply, before a single ounce reaches jewelry, industrial, or private investment demand. The World Gold Council survey found that 95% of central banks plan to increase their gold reserves in 2026 — the 17th consecutive year of net official sector purchases. This demand does not pause when the Strait of Hormuz opens. It does not decelerate when oil prices fall. It is structural, multi-decade reallocation of sovereign wealth away from fiat currencies and into the only asset with no counterparty risk.

Price Targets and the Road to $5,000+

Goldman Sachs raised its year-end 2026 gold price target to $5,400 per ounce, citing central bank purchases of approximately 60 tonnes per month as a primary driver. JPMorgan projects gold pushing toward $5,000 per ounce by Q4 2026, with $6,000 a possibility longer term. These projections were made before the Hormuz crisis began adding a geopolitical risk premium that, even partially deflating as it is today, is providing a floor for prices at $4,700-$4,870 heading into the weekend.

Today's market dynamic illustrates a concept professional gold analysts call the asymmetric bid structure. When geopolitical risk rises, gold surges. When geopolitical risk partially resolves, gold holds and then advances on the monetary policy tailwind created by lower energy prices and reduced inflation. Gold is positioned to benefit in multiple scenarios simultaneously, a characteristic that makes it uniquely valuable in environments where uncertainty itself is the dominant market condition.

.png)

Five Reasons Gold Wins in Both Scenarios

1. Hormuz Stays Open — The Rate Cut Pathway

Lower oil prices reduce headline CPI by 0.5-1.0 percentage points within two quarters. A Fed that was paralyzed by energy-driven inflation suddenly has room to cut. Real interest rates fall. The dollar weakens. Every historical Fed easing cycle has coincided with gold strength. With Goldman Sachs and JPMorgan both projecting $5,000-$5,400 gold even in the benign scenario, the floor under prices is structural, not speculative.

2. Hormuz Re-Closes — The Safe Haven Surge

Any breakdown in ceasefire talks, any provocative act by either side, any resumption of U.S. or Israeli military operations sends oil back above $100 and gold through $5,500 or higher. The Motley Fool reported directly today that the strait could close again if a final peace deal is not reached, with Goldman Sachs maintaining a Brent stress case of $115 per barrel. Physical gold held in a Precious Metals IRA is the only asset that rises in this scenario while most portfolios bleed.

3. Central Bank Demand Does Not Stop for Geopolitics

The 755-tonne central bank purchase projection for 2026 reflects structural reserve diversification decisions made over multi-year planning horizons. Poland's explicit target of 20% gold in national reserves, China's 16-month buying streak, Uzbekistan emerging as the largest buyer in January 2026 — these are not momentum trades. They are permanent shifts in sovereign reserve architecture. This demand absorbs 25% of annual mine supply before retail investors buy a single coin.

4. Fiscal Deficits and Dollar Debasement Are Unresolved

The U.S. federal interest expense is projected to exceed $1.1 trillion in 2026, absorbing 19% of all federal tax revenue. The national debt approaches $38 trillion. The dollar has lost 3% in three consecutive weekly declines, with the DXY at one-month lows today. These structural realities exist entirely independent of the Strait of Hormuz. Fiat currency debasement has been the multi-decade driver of gold, and no ceasefire resolves a $2.1 trillion annual federal deficit.

5. The Inflation Floor Remains Above Target

Even with oil prices falling 11% today, core inflation remains above 3%. The Fed's own 2026 PCE forecast has been revised up to 2.7%. Shelter, services, and core goods continue to show stickiness. A ceasefire removes the energy shock but does not reset the structural inflation dynamics that have been brewing since 2021. Gold performs in environments of persistent above-target inflation regardless of energy price direction.

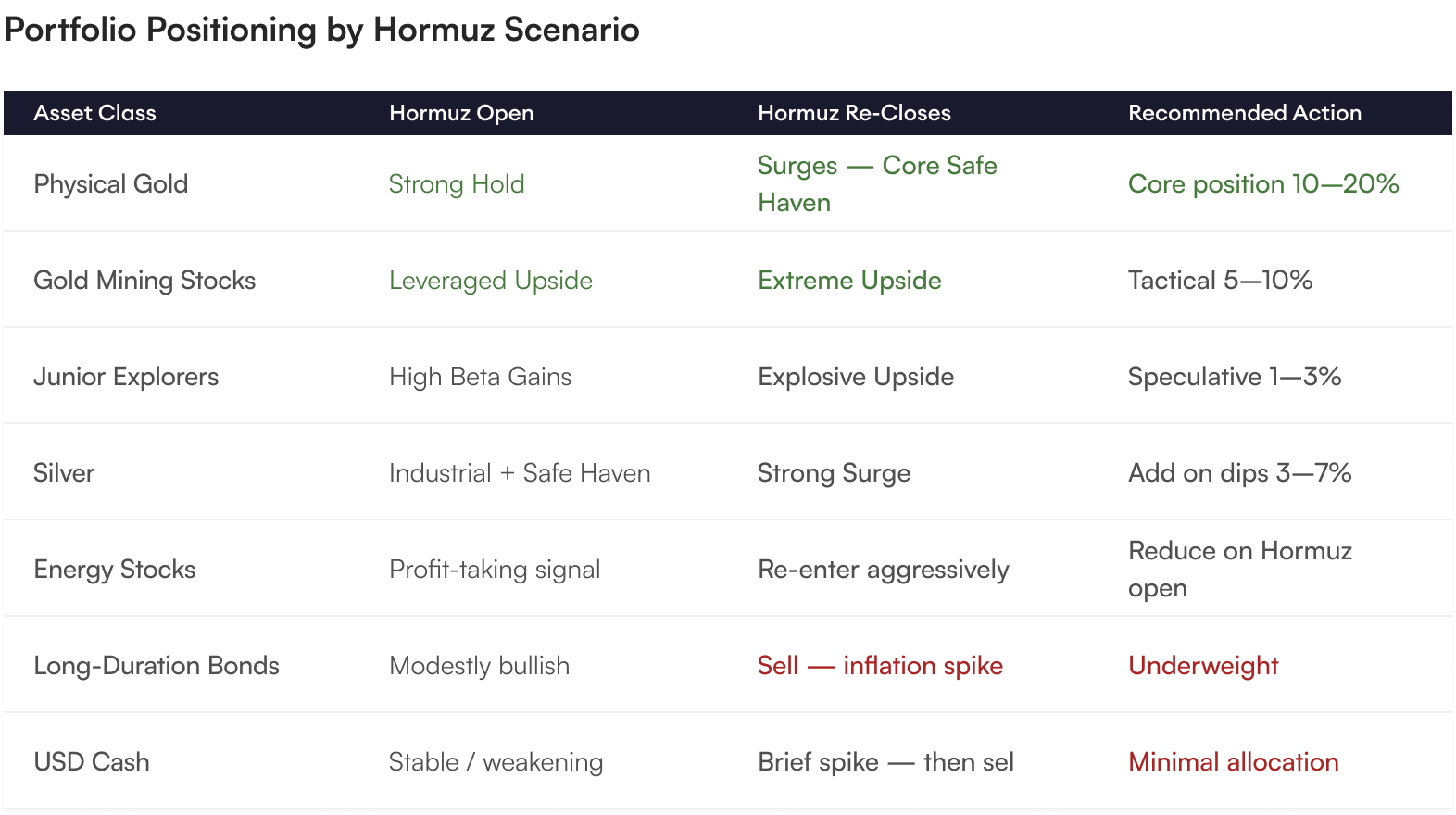

Portfolio Strategy: Positioning for the Hormuz Reset

Today's developments require a recalibration of precious metals portfolio positioning — not a wholesale change, but a thoughtful adjustment that accounts for the shift from pure crisis-driven demand to a blend of monetary, fiscal, and residual geopolitical tailwinds. The following framework is designed for retirement investors who want to align with the most informed institutional capital in the world.

The Three Questions Every Retirement Investor Must Answer

Before this weekend, every retirement investor should honestly assess their portfolio against three questions that the Hormuz crisis has made impossible to ignore:

- If the ceasefire collapses next week and oil surges back above $100, what percentage of my portfolio benefits rather than suffers?

- If the ceasefire holds, the Fed cuts rates twice in 2026, and gold advances to $5,400 as Goldman Sachs projects, what percentage of my portfolio participates in that gain?

- If both scenarios play out over 18 months, alternating between crisis and relief, with gold rising in both directions, what is my current allocation to the only asset that performs in both?

If the answer to any of these questions is zero or near zero, today's Hormuz opening is your reminder that geopolitical events can move at a pace that leaves under-positioned investors no time to react. The investors who are positioned in physical gold today are watching their holdings rise 1.67% on a day when oil collapsed. That is the power of owning the monetary metal that 95% of the world's central banks are currently accumulating.

Act Before the Next Chapter Begins

The Strait of Hormuz reopening is a pause in a geopolitical crisis that has not been resolved. It is a ceasefire, not a peace treaty. It lasts as long as the Lebanon ceasefire holds, and the U.S. naval blockade remains in place. The next development, whether a breakdown in talks or a final peace agreement, will move markets sharply in one direction or another. Physical gold is the only asset positioned to benefit in multiple outcomes.

Contact Merchant Gold Group Today

Position your retirement portfolio alongside the world's most informed institutional gold buyers