Most American investors who own gold today own it through an exchange-traded fund. ETFs are convenient, liquid, and easy to buy in any brokerage account. They are also taxed in a way that quietly costs investors a meaningful share of their long-term return — a fact that is rarely mentioned in the marketing copy, and one that retirees in particular ought to understand before assuming paper gold is equivalent to physical gold.

The good news is that the most common workaround is straightforward, fully IRS-approved, and accessible to almost any saver with an existing retirement account.

The Collectibles Tax Most ETF Holders Don't Know About

Under current U.S. tax law, gains on physical gold and on most gold-backed ETFs held outside of retirement accounts are taxed as collectibles when held longer than one year. The maximum federal long-term capital gains rate on collectibles is twenty-eight percent, compared with the twenty percent maximum that applies to most stocks and stock funds. State taxes apply on top of that. For a high-bracket investor, the difference between the two regimes can shave a meaningful percentage off the after-tax return on a multi-decade position.

That collectibles treatment applies whether you hold physical bullion in your home or shares of a popular gold ETF in a taxable brokerage account. The IRS treats them similarly for capital gains purposes, even though the legal structures are completely different. The result: the tax efficiency many investors believe they are getting from a paper product simply is not there.

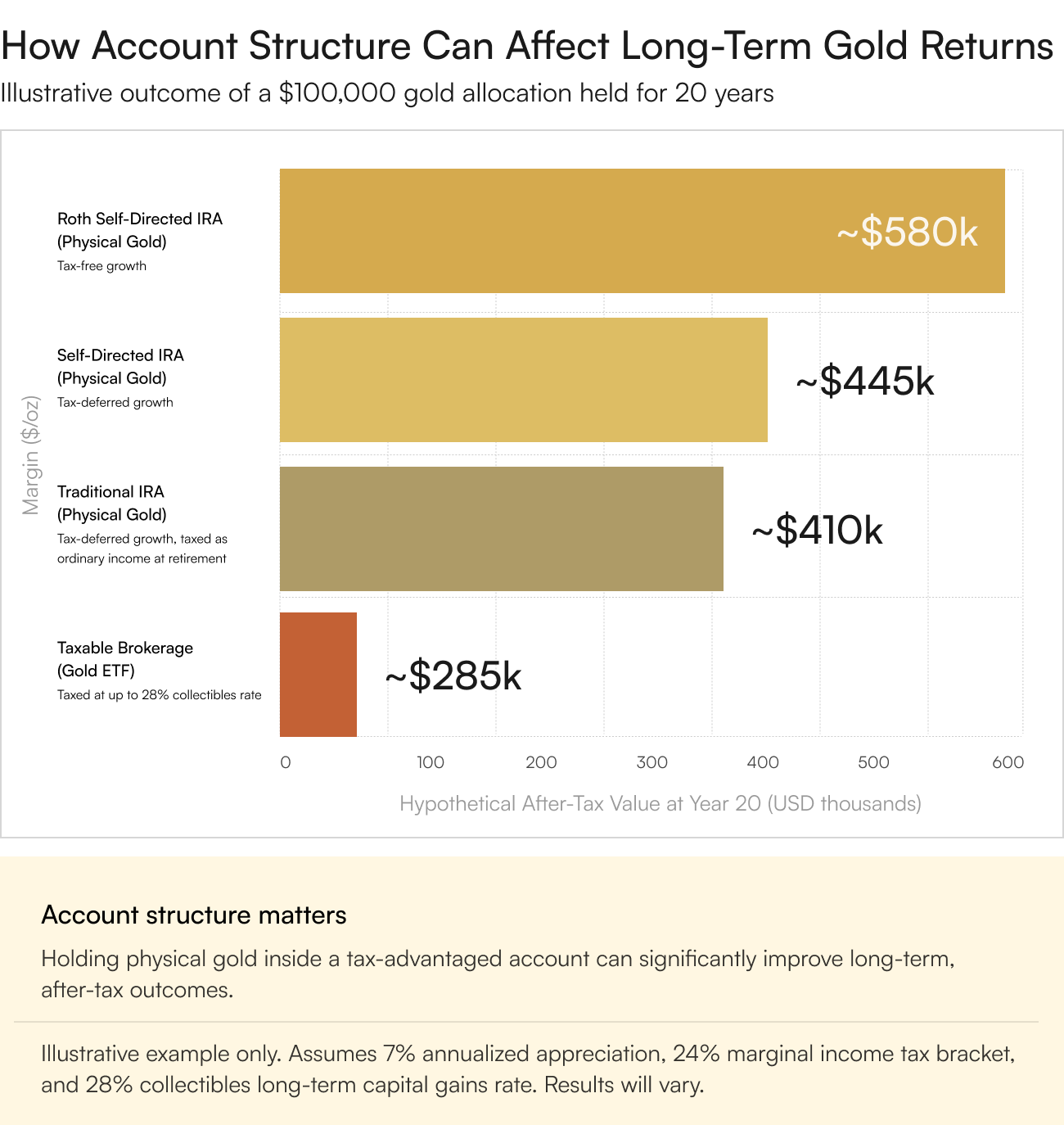

How a Self-Directed Precious Metals IRA Changes the Math

A self-directed IRA is a retirement account that allows the holder to invest in a wider range of assets than a typical custodian permits — including physical gold, silver, platinum, and palladium, as long as the products meet IRS fineness standards and are stored at an approved depository.

Inside an IRA, the collectibles rate disappears. Gains compound tax-deferred in a traditional self-directed precious-metals IRA, and tax-free in a Roth version. Distributions from the traditional account are taxed as ordinary income at retirement, while qualifying Roth distributions come out untaxed entirely. For a long-horizon holder of physical metals, the IRA wrapper is the most tax-efficient structure available under current law.

“If you're going to own gold for twenty years, the question isn't really whether to own it — it's where to hold it. The wrapper around the asset can be worth more than the asset's nominal return.” — Retirement planning commentary

How the Rollover Actually Works

Most savers who establish a precious-metals IRA do so by rolling over funds from an existing 401(k), 403(b), or traditional IRA. The mechanics are well-established: the existing custodian transfers funds directly to the new self-directed IRA custodian, the saver selects IRS-approved bullion products, and the metals are shipped to a qualifying depository for storage. No taxable event is triggered if the rollover is executed properly.

The investor retains full ownership of specific physical metals — not a pooled claim, not a paper proxy. They can be inspected, audited, and ultimately distributed in kind at retirement, or sold and the proceeds distributed as cash. The same IRS rules that govern the rest of an IRA — required minimum distributions, contribution limits, beneficiary designations — apply normally.

What to Look for in a Custodian and Dealer

Three things matter most. First, transparency on fees: a reputable dealer publishes clear pricing on bullion products and clear setup, transaction, and annual storage fees. Second, IRS-approved storage: the depository must be qualified under IRS rules, fully insured, and capable of segregating client metal on request. Third, real specialists on the phone: the firm guiding you through the paperwork should explain rules accurately, not push numismatic coins or pressure you toward a single product.

The mechanics of opening the account are straightforward. The work that matters is selecting a dealer and custodian that treat the relationship as a long-term one, because the account itself will likely outlast most other relationships in your financial life.

Practical steps for you.

The right account structure can quietly add years of effective return to a long-horizon precious-metals position — at zero additional risk. To explore whether a rollover into a self-directed precious-metals IRA fits your retirement plan, schedule a consultation with Merchant Gold Group and walk through the process step by step with a real specialist who answers questions plainly.