.png)

The U.S. housing market is showing clear signs of cooling as mortgage rates have surged past the 7% threshold for the first time in over two decades. This rise in borrowing costs is prompting many prospective buyers to rethink their timing and affordability, leading to slower home sales and moderating price gains across many regions.

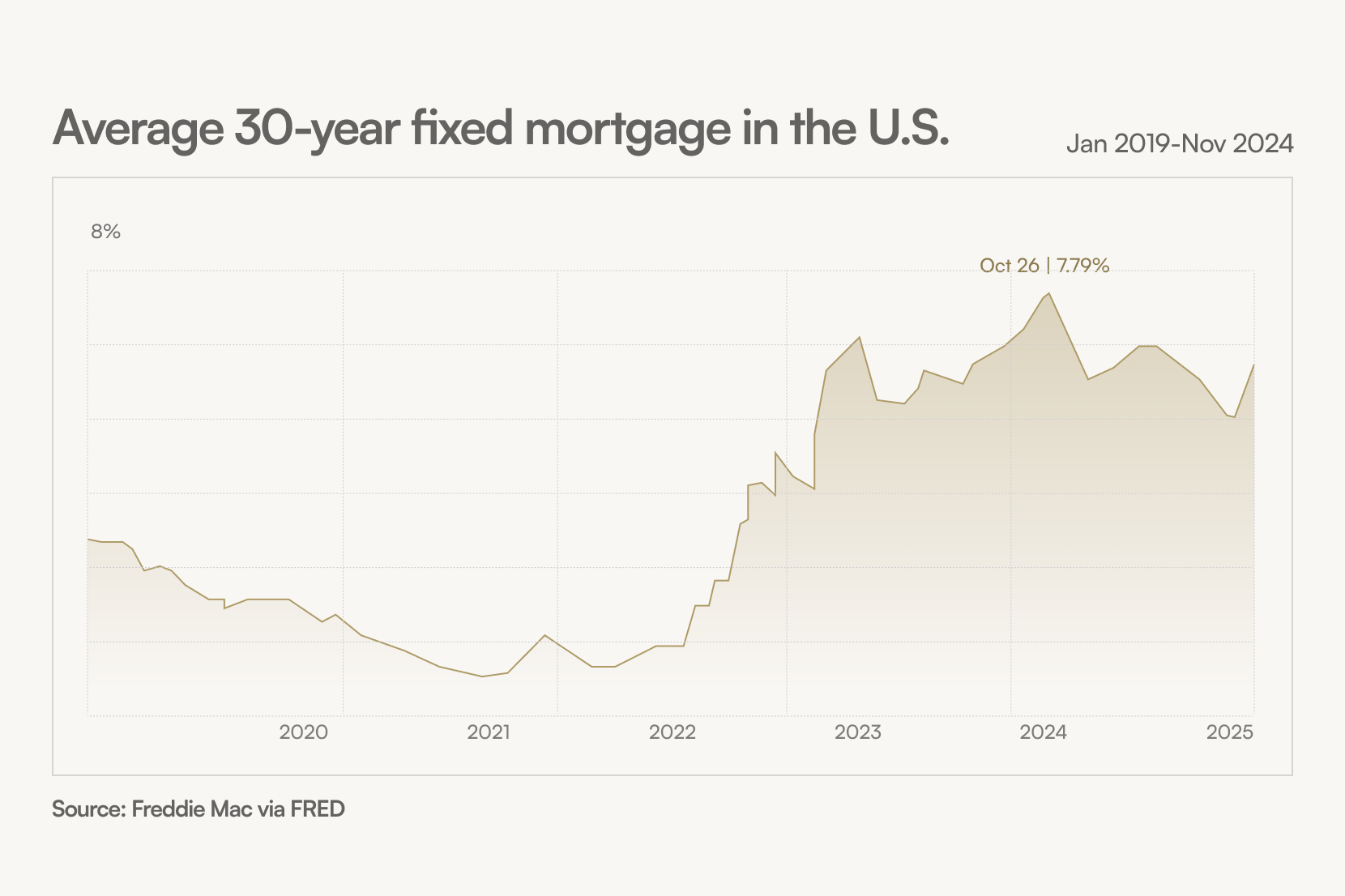

Mortgage Rates Reach a New High

According to Freddie Mac, the average 30-year fixed mortgage rate recently climbed to 7.1%, levels unseen since the early 2000s. This dramatic increase from sub-3% rates during the pandemic has fundamentally shifted the housing affordability landscape. Rising interest rates translate into substantially higher monthly mortgage payments. For example, on a $400,000 home loan, moving from a 3% to 7% rate increases the monthly payment by nearly $1,200, putting homeownership out of reach for many buyers. Lydia Chen, chief economist at Evergreen Housing Analytics, explains: "Higher rates are pricing out a segment of buyers, especially first-timers and moderate-income households, who were already challenged by high home prices. This is slowing sales and prompting a pullback in market activity."

Slowing Sales and Price Stabilization

Data from the National Association of Realtors (NAR) highlights a 5.4% month-over-month drop in existing home sales in April 2025, marking the fourth consecutive monthly decline. New home starts have similarly slowed, with the U.S. Census Bureau reporting a 7% reduction compared to the previous quarter. While home prices remain elevated, there are early signs of stabilization and even modest declines in some overheated markets. Cities like Phoenix, Austin, and Miami — which saw double-digit price gains in recent years — are now experiencing year-over-year price growth closer to zero or even slight contractions. This moderation signals a shift from the seller’s market of recent years toward a more balanced environment where buyers have greater negotiating power.

Regional Differences in Market Impact

The housing slowdown is not uniform across the country. High-cost coastal cities like San Francisco, New York, and Boston continue to see relatively resilient demand, supported by limited inventory and strong local economies. Conversely, more affordable markets in the Midwest and Southeast are feeling the impact of higher borrowing costs more acutely. Regions such as Cleveland, St. Louis, and Atlanta are reporting steeper drops in sales volume and slowing price appreciation. Suburban and exurban areas that benefited from pandemic-era migration are also seeing buyer interest wane as affordability pressures mount and remote work policies evolve.

Buyer Behavior Adapts to New Realities

The rise in mortgage rates has led to significant shifts in buyer behavior. Many prospective homeowners are delaying purchases, opting instead to rent longer or reconsider their home size

and location preferences. Some buyers are exploring adjustable-rate mortgages (ARMs) or interest-only loans as alternatives to fixed-rate mortgages, seeking lower initial payments with the risk of future rate

increases. Others are turning to more affordable housing types, such as condos and townhomes, or expanding their geographic search to less expensive suburbs and rural areas. Homebuyers are also increasingly sensitive to total monthly costs, including taxes and insurance, in addition to the principal and interest payments.

Sellers Adjust Pricing and Incentives

On the selling side, homeowners and developers are beginning to adjust their expectations. After years of rapid price appreciation, many sellers are moderating asking prices and offering concessions such as closing cost assistance, home warranties, or flexible move-in dates to attract buyers. Real estate agents report longer listing times and increased negotiation between buyers and sellers, which had been rare during the pandemic-fueled boom. Builders, facing higher financing costs and cautious buyer demand, are focusing more on entry-level and mid-priced homes, while delaying or downsizing luxury developments.

Long-Term Market Outlook

Looking ahead, the housing market is expected to remain more subdued than the explosive growth seen from 2020 to early 2023. Elevated mortgage rates, combined with persistent affordability challenges, will likely keep sales activity below historical averages for some time. Demographic trends, such as the large millennial generation entering peak homebuying years and ongoing urbanization, will support steady demand over the longer term. However, supply constraints—particularly in affordable housing segments—could limit price declines. Economic factors like wage growth, inflation, and labor market health will also be key to the housing market’s trajectory. Should inflation ease further and wage gains accelerate, affordability may improve modestly. Moreover, any shifts in Federal Reserve policy or mortgage lending standards could influence market dynamics.

Key Takeaways for Buyers and Sellers

- Buyers: Higher rates mean careful budgeting and mortgage shopping are critical.

Exploring different loan products, expanding geographic searches, and considering

smaller homes can help navigate affordability challenges. - Sellers: Pricing homes competitively and offering incentives can help attract cautious

buyers. Working with knowledgeable real estate professionals is more important than

ever to manage expectations. - Investors: Real estate investors may find opportunities in rental markets as some

buyers delay purchases, but they should monitor interest rate trends and local market

conditions carefully.

As the market recalibrates, homebuyers and sellers alike must adapt to a new environment defined by higher financing costs and evolving economic conditions. While the housing boom has cooled, the market remains a crucial component of the broader economy and a key area to watch in the months ahead.