U.S. national debt crossed thirty-seven trillion dollars in early 2026, less than two years after first crossing thirty-five trillion. The number itself is so large it has lost most of its meaning to ordinary observers, and that may be the most dangerous part. A debt level that produces a shrug today would have produced a national emergency a generation ago, and the underlying mechanics that drive household purchasing power have not changed — only the willingness of policymakers, markets, and savers to look at them.

This is not a political article. It is an article about arithmetic. The arithmetic of sovereign debt is not partisan, and the implications for a retiree's savings are not partisan either.

Why the Debt Number Matters to a Household

The U.S. government services its debt through a combination of tax revenue, new borrowing, and — when those become insufficient — accommodative monetary policy that effectively monetizes a portion of the obligation. Each of those three levers has limits, and as debt grows relative to GDP, those limits tighten. Annual interest payments on the federal debt now exceed defense spending and rival Social Security in size, mechanically squeezing the rest of the federal budget.

For a household, the relevance is indirect but real. A government that depends on accommodative monetary policy to roll its debt creates conditions that erode the purchasing power of currency-denominated savings — bank deposits, money market funds, intermediate-duration Treasuries, and most pensions and annuities. The nominal balance does not change. The amount of real-world goods and services that balance can buy does.

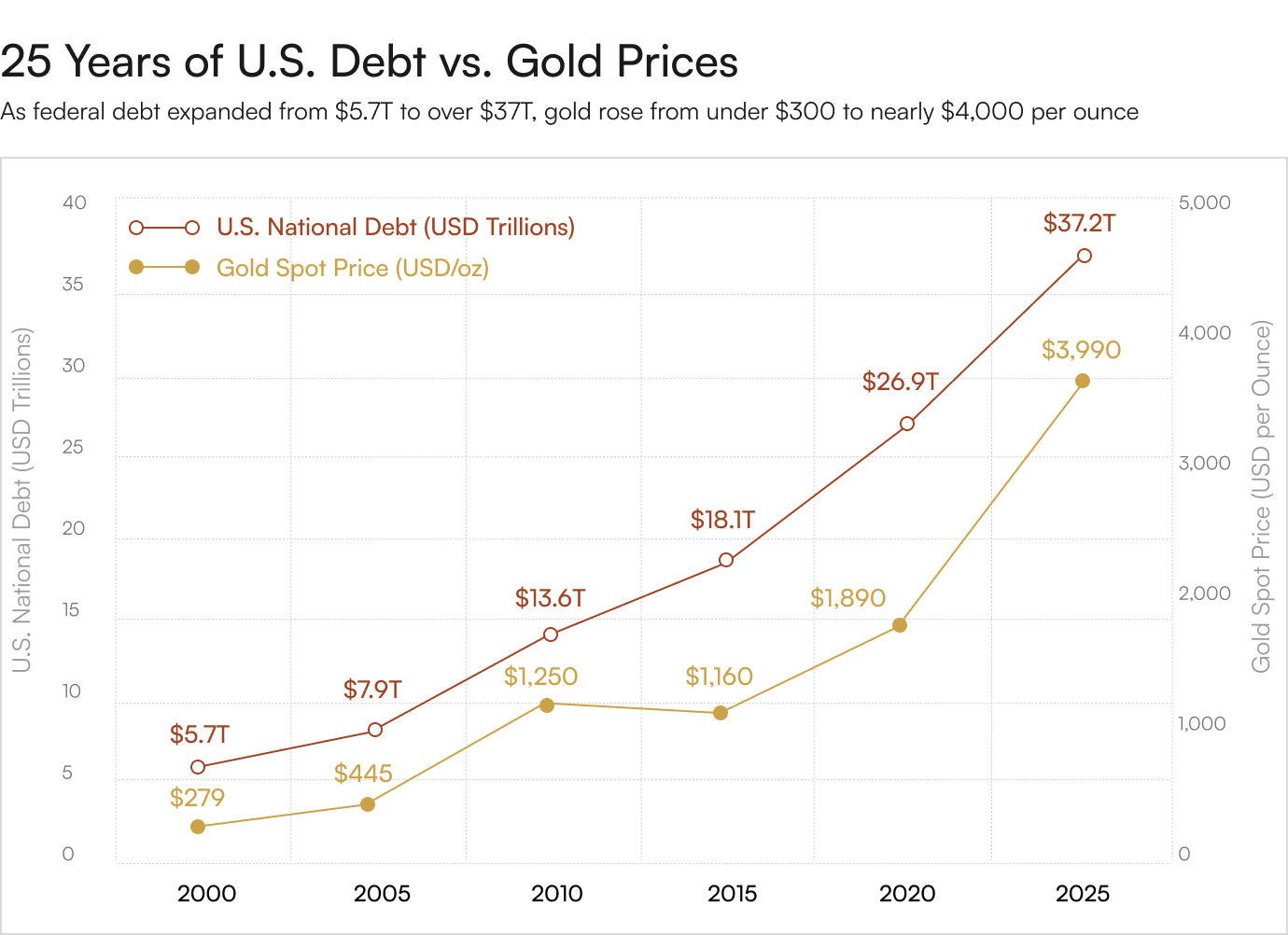

A Pattern That Has Repeated for 25 Years

Over the past quarter century, U.S. debt has expanded from roughly five trillion dollars to nearly thirty-eight trillion. Over the same period, gold has moved from approximately two hundred and seventy dollars per ounce to a 2026 peak just under five thousand six hundred dollars per ounce. That is not a perfect month-to-month correlation, and there have been multi-year periods in which gold has gone sideways or fallen. But across the full window, the relationship is unmistakable: as the dollar denominator has grown faster than the gold supply, the price of gold in dollars has had to mathematically respond.

None of this is mysterious. Gold mine supply grows at roughly one to two percent per year. The U.S. monetary base and federal debt have expanded at multiples of that rate over the same span. The ratio of dollars to gold ounces has been steadily rising, and the price has, in fits and starts, reflected that ratio. There is no reason to expect the underlying dynamic to reverse on any timeframe relevant to a retirement plan.

“The deficit is not the problem; the deficit is the symptom. The problem is that there is no political constituency for fiscal restraint, and there hasn't been for two decades.” — Economic policy commentary

What This Means for the Savings Side of the Ledger

Households have three primary defenses against a debt-driven inflation regime. The first is owning productive assets — equity in real businesses with pricing power. The second is owning hard assets — real estate, commodities, and precious metals — that retain value as currency loses it. The third is accepting the loss in real terms by holding nominal instruments and watching purchasing power erode quietly.

Most American retirees are heavily concentrated in the third category through bond holdings, fixed annuities, and cash equivalents. A modest reallocation toward hard assets — particularly physical gold, which has the longest empirical track record of preserving purchasing power across debt-driven currency cycles — is not a speculative bet on a single price target. It is a structural defense against a slow, predictable form of loss.

Why Physical Holdings Matter More Than Paper Proxies

In a debt-stress environment, the assets that historically hold up are the ones with no counterparty. Physical gold held by the owner, or held by a credible third-party depository under the owner's name, is not subject to a bank's solvency, a fund sponsor's redemption policy, or a brokerage's custodial chain. It does not require the financial system to be working in order to retain value — which is precisely the conditions under which it has historically delivered the most outperformance.

Paper exposure to gold offers the upside but reintroduces the counterparty risk gold was added to remove. For investors who are buying the asset to hedge the system, the wrapper matters.

Where should you buy gold

Sovereign debt arithmetic is one of the few financial variables that genuinely is predictable on multi-decade timeframes, and prudent savers plan for it rather than around it. If you would like a clear, no-pressure conversation about how a measured physical-metals allocation can sit alongside your existing retirement and brokerage holdings, speak directly with a Merchant Gold Group advisor — they will walk you through IRS-approved options and answer questions in plain language.